The Liquidity Layer: Why Liquidity Is the Real Utility of Digital Finance

Liquidity’s transformation: why the line between traditional and decentralized markets is blurring—and what it means for investors.

Editor’s Note: This piece is part of The RWA Ledger’s series on how liquidity, regulation, and infrastructure are converging across TradFi and DeFi.

When Liquidity Becomes the Market

Liquidity has long been the financial world’s oxygen: invisible, all-encompassing, and instantly indispensable when it starts to vanish. In 2021, a tidal wave of nearly $9 trillion in global stimulus didn’t just buoy asset prices; it fueled speculative frenzies from meme stocks to NFTs, making liquidity the star rather than the stagehand.

By 2025, the landscape will have undergone a fundamental change. Liquidity is no longer just a side effect of stimulus; it is now the very framework upon which markets are built. What was once a background variable has evolved into the backbone of modern finance; programmable, quantifiable, and enforced as much by algorithms and policy as by capital flows.

For institutional investors, liquidity is no longer an abstract force; it is engineered, managed, and actively shaped. In this new era, it acts less like a feature and more like the hidden circuitry of the market itself.

“Liquidity isn’t a market feature; it’s the market’s hidden architecture.”

The Hidden Architecture of Liquidity

On Wall Street, liquidity is often reduced to a matter of available cash. But the reality is far more intricate. Liquidity is the unseen plumbing of global finance, the network of valves, reservoirs, and conduits engineered to keep capital flowing. Central banks, repo desks, primary dealers, and money market funds together form an interconnected system that quietly underpins every trade and transaction.

On October 31, 2025, the U.S. Federal Reserve’s Standing Repo Facility (SRF) surged to a record $50 billion in usage, a spike that didn’t go unnoticed by seasoned Treasury traders. Beneath the headlines of economic stability, this was a warning signal: liquidity reservoirs were running shallower than official narratives suggested. Unlike quantitative easing, where monetary largesse is spelled out for all to see, the SRF operates in the background, injecting overnight liquidity surreptitiously to unclog market blockages. Think of it as “stealth QE”, policy support folded discreetly into market infrastructure.

Former BitMEX CEO Arthur Hayes described it bluntly:

“If SRF balances are above zero, then we know the Fed is cashing the checks of politicians using printed money.”

Hayes’s perspective, provocative as it may be, highlights a broader shift. Today, liquidity is no longer simply the result of policy choices; it has become embedded, structural, and algorithmic. As volatility and funding stress emerge, liquidity pulses through the system by design, not decree. The infrastructure now thinks and reacts in real-time, adjusting flows as if the market itself had developed a circulatory system.

In this new era, liquidity is more than a lever. It’s the market’s silent engine, always running, rarely observed, and essential.

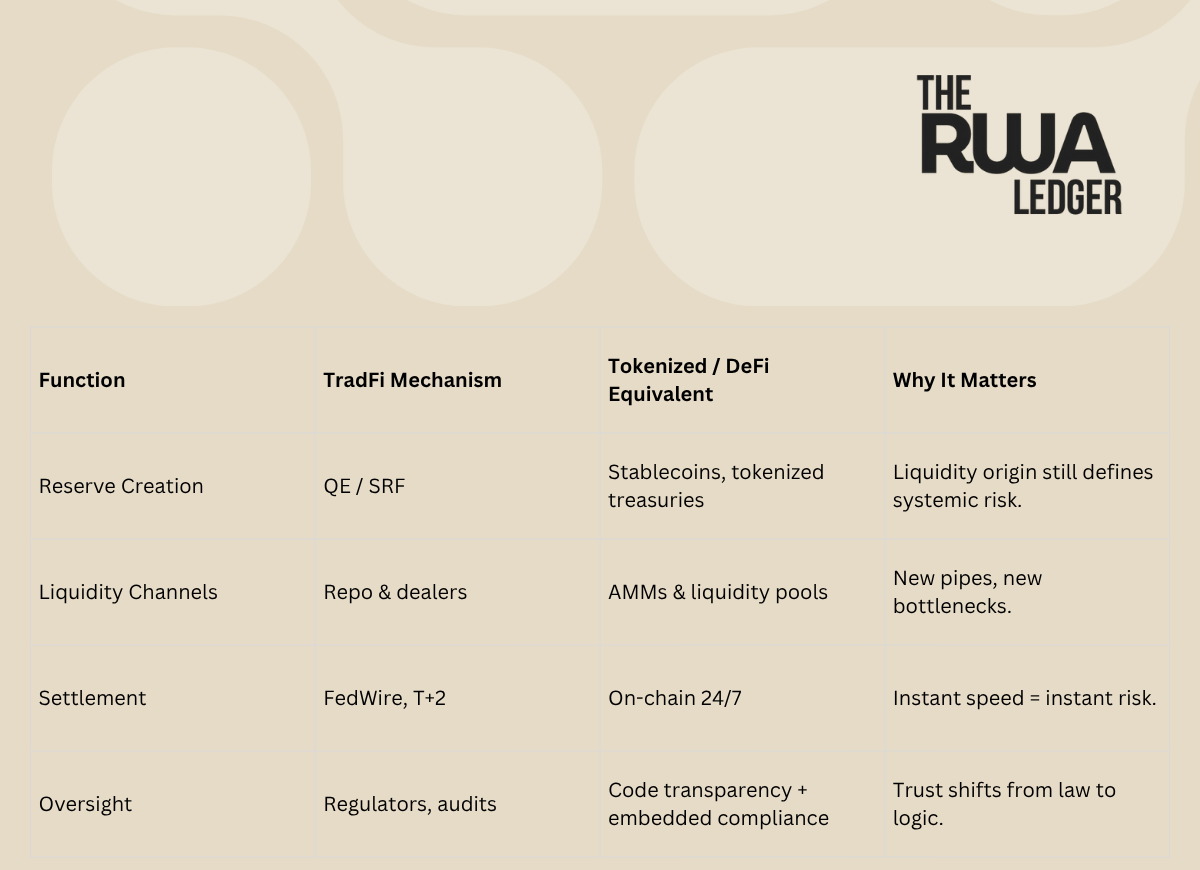

How liquidity flows in TradFi:

Think of liquidity in traditional finance as a carefully balanced chain:

Central bank → commercial bank → repo → corporate credit → market assets.

Every link matters. Disrupt the flow at any point, be it central bank policy, repo market hiccups, or pressure on corporate credit, and the impact ricochets across the entire system. A swelling Treasury General Account can drain reserves from banks, spark a spike in repo rates, and tighten conditions even for the safest borrowers. Each node amplifies risk, revealing just how intertwined and fragile the system can be.

Liquidity’s effects remain largely unseen, but they are never theoretical. When balance sheets expand, risk assets predictably surge, equities climb, bond yields compress, and even tokens in digital markets benefit. The transmission of liquidity is silent, but its consequences shape every portfolio and asset class.

In today’s interconnected markets, liquidity isn’t just a back-end process; it’s a sensitive, systemic pulse connecting every layer of finance.

Liquidity Across Systems: From Balance Sheets to Blockchains

The tightly connected flows of traditional finance reveal just how sensitive the entire system is to liquidity disruptions, yet this complexity hasn’t vanished with the dawn of digital markets. Instead, the very concept of liquidity is being rewritten. As capital marries code and infrastructure crosses into programmable territory, liquidity management shifts from physical pipes to digital rails, without abandoning its foundational logic.

Tokenization doesn’t replace the core plumbing of liquidity; it re-codes it. The players may be new and the velocity of movement noticeably faster, but the fundamental constraints endure. The chain from reserves to market assets persists - only now, each link can be engineered in software, monitored in real time, and governed by both policy and protocol.

TradFi → Tokenized flow:

This new architecture transforms liquidity into something closer to living software, adaptive, predictive, and always on. As TransOcean Lab writes:

“When liquidity is unified, markets start to behave like one continuous system, not disconnected fragments.”

The limitations of early DeFi, most notably, capital locked in static pools, are giving way to the next wave: “liquidity that can think.” Markets are evolving towards intelligent, self-balancing systems, where capital responds to spreads, volatility, and depth in real time.

The future of money is defined by liquidity intelligence: programmable, transparent, and capable of spanning both balance sheets and blockchains. This evolution isn’t just about technology; it’s about the logic and resilience of the market itself.

The new monetary logic is characterized by liquidity intelligence, being predictive, programmable, and transparent.

The Liquidity Illusion: Tokenization’s Promise and Its Limits

As the machinery of liquidity migrates from traditional to digital finance, a powerful narrative has emerged: “tokenization unlocks liquidity.” It’s an alluring promise, and one of the most persistent misconceptions in the space.

As Emma Channing puts it succinctly:

“The mere act of tokenizing an asset does not make it liquid.”

In reality, tokenization brings possibility, not inevitability. Turning an asset into a digital token may widen access and visibility, but it does not guarantee the presence of buyers and sellers. Market structure fundamentals endure: for every transaction, you still need market makers to provide depth, price discovery to anchor value, and regulatory clarity to instill confidence. Potential liquidity is not the same as an active market.

Traditional finance, or “TradFi,” relies on layers of regulated intermediaries to maintain reliably liquid markets. In decentralized finance, that scaffolding is swapped for code and incentives: automated market makers, liquidity pools, and protocols like Uniswap or Curve. They attract capital through mechanisms, such as LP tokens, fee distributions, and yield farming schemes, but these are incentives, not mandates. The invisible hand must still be enticed to act.

The lessons of TradFi persist. The same risks that drive volatility and stress in repo markets—slippage, herd behavior, and a sudden flight to safety—are equally present in tokenized environments. Liquidity is a moving target, never static or automatic. It must be maintained, not just manufactured. Several constraints shape the proper supply of liquidity, regardless of the technology layer:

Several constraints shape the proper supply of liquidity, regardless of the technology layer:

Demand: Fractionalizing assets may lower barriers, but it does not conjure buyers.

Market makers: There are a few firms capable of quoting real-world assets (RWAs) at a global scale.

Regulation: Stringent KYC/AML requirements can impede spontaneous flows.

Valuation: Price discovery in tokenized assets often lags underlying NAVs, widening bid-ask spreads and eroding confidence.“Liquidity can’t be tokenized into existence — it must be earned and kept.”

As Upside.gg’s primer reminds us:

“LP tokens act like balancing mechanisms and provide a sense of security to investors for the assets they deposit.”

Still, security alone does not create liquidity. The infrastructure is necessary, but not sufficient. In any context, liquid markets must be built, tended, and trusted.

In short, liquidity can’t be programmed into existence. It must be earned, and continually kept.

Policy as Infrastructure: Regulation and Systemic Liquidity

As liquidity evolves from silent enabler to explicit infrastructure, it has also become a lever of policy and a flashpoint for geopolitical strategy. Tokenization and stablecoins are now recognized as more than financial innovations; they are national-security priorities.

As Susan Joseph (Cornell) and Broadridge assert, these technologies form “the connective tissue between traditional and modern financial systems.”

The old backbone of finance relied on curated windows and measured processes: FedWire’s limited hours, T+2 settlement periods, and end-of-day risk checks. These rails were designed for a daylight economy, where liquidity could be monitored and dialed with intent. In stark contrast, tokenized systems operate at all hours, subjecting markets to a new vulnerability, instantaneous flows in the absence of round-the-clock regulation.

Joseph warns that:

“Current financial infrastructure cannot handle 24/7 instant liquidity.”

This risk is pushing regulators to redirect their focus. The debate is quickly shifting from how to regulate crypto assets to how to regulate liquidity itself. What matters now is the architecture of oversight; policies must be “fit-for-purpose, light-touch,” able to adapt as fast as technology. The question is no longer if regulation should evolve, but how quickly it can keep pace with programmable, borderless liquidity.

Data highlights how deeply integrated these flows have become. S&P Global finds a strong correlation of +0.75 between M2 growth and digital-asset performance since 2017, as well as a negative correlation of –0.33 with interest rate hikes. As the boundary between TradFi and DeFi erodes, so too does the insulation against market shocks; events in one system ripple instantly across the other.

Against this backdrop, regulators’ priorities crystallize:

Transparency: Can every digital flow be continually audited?

Resilience: Are markets designed to withstand macroeconomic stress in real-time?

Accountability: Can compliance be built into the infrastructure to ensure legal traceability?

The truth is clear: liquidity may now move at code speed, but trust, regulation, and systemic safety still travel at the speed of law. Bridging this gap will define the next chapter for global markets.

The Intelligent Liquidity Era

The nature of liquidity is transforming, no longer just a static balance-sheet artifact, but a living, adaptive software layer embedded into the fabric of global markets. We’ve entered the age of “liquidity intelligence,” where capital flows are not only measured and monitored but also predicted, optimized, and automatically corrected in real-time.

TransOcean Lab aptly describes this as liquidity that learns, able to anticipate stress, reallocate seamlessly, and balance risk autonomously. Leading institutions are bringing this vision to life: BlackRock’s BUIDL Fund and Franklin Templeton’s OnChain Government Money Fund showcase tokenized treasuries as modern reserve instruments. Citi’s “Tokens, Money & Games” report and J.P. Morgan’s Onyx program position tokenization as the new foundation for private markets. Meanwhile, the BIS and Checkout.com are pioneering programmable settlement and compliance, turning monetary operations into real-time, coded logic.

Yet, with these advancements comes a new governance imperative. As markets become more composable and operate around the clock, policy and oversight must evolve just as rapidly.

Christine Lagarde’s warning is timely: “Stablecoins, particularly those that have the potential to reach a global scale, pose serious risks to financial stability, monetary policy transmission and the smooth functioning of payment systems.”

Our infrastructure is now continuous, meaning regulation, risk management, and market responses must be, too.

We have entered an era where:

Liquidity behaves like software: endlessly programmable and adaptive to shocks.

Regulation becomes infrastructure: compliance and execution merge as native components of code.

Continuous markets demand continuous oversight: policy must keep pace with markets that never close.

Ultimately, the next frontier in market advantage won’t simply be holding more liquidity, but rather wielding smarter liquidity—capital that is intelligent, resilient, and ready for the systemic paradigm ahead.

As Broadridge and Cornell conclude,

“The next market advantage won’t be who has more liquidity, but who has smarter liquidity.”

Key Takeaways

Liquidity has become an infrastructure, not just a stimulus.

Tokenization re-codes existing flows but doesn’t erase old constraints.

Deep markets remain a bottleneck; liquidity does not always equal depth.

Law and code are merging into a unified operating standard.

TradFi and DeFi liquidity correlations are strengthening, binding the old and new systems together ever more closely.

Looking Ahead

Next in The RWA Ledger:

“Regulation as Infrastructure | When Policy Becomes the Market Framework.”

Marina Mendenhall-Valente

Partner, Tiburon Advisory Group | Founder of

Bridging TradFi × DeFi Through Emerging Tech

Views are my own. This publication is for informational purposes only and does not constitute financial advice, endorsement, or investment solicitation.

So true…”

The old backbone of finance relied on curated windows and measured processes: FedWire’s limited hours, T+2 settlement periods, and end-of-day risk checks. These rails were designed for a daylight economy, where liquidity could be monitored and dialed with intent. In stark contrast, tokenized systems operate at all hours, subjecting markets to a new vulnerability—instantaneous flows in the absence of round-the-clock regulation.”