The Death of the Roll

How Perpetual Futures Are Rewriting the Rules of Capital Efficiency

Wall Street closes its doors at 4:00 PM, but the global financial landscape no longer sleeps. For decades, legacy equities futures have stood as the bedrock of institutional hedging, shackled by rigid trading hours and manual rollover friction. But a revolution is underway.

Every financial innovation promises to reduce friction. Very few eliminate an entire category of it. Perpetual futures may be one of those rare exceptions.

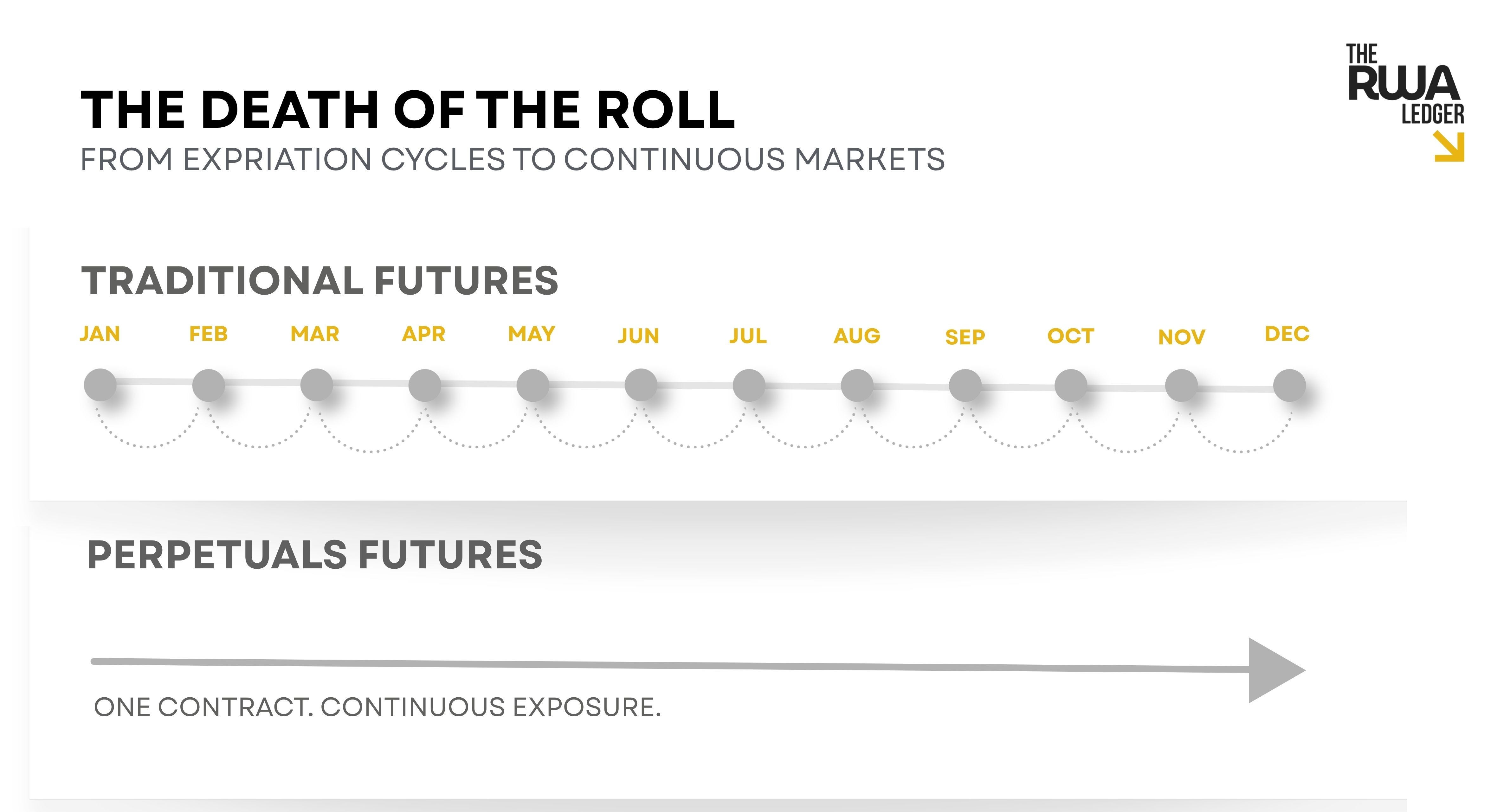

The traditional futures market has a major flaw: it expires.

Markets do not merely price assets. They price time. Traditional futures embed time directly into the contract, forcing participants to constantly look toward a calendar deadline. By removing expiration dates altogether, perpetual futures allow capital to remain deployed instead of being repeatedly reset through contract rollovers.

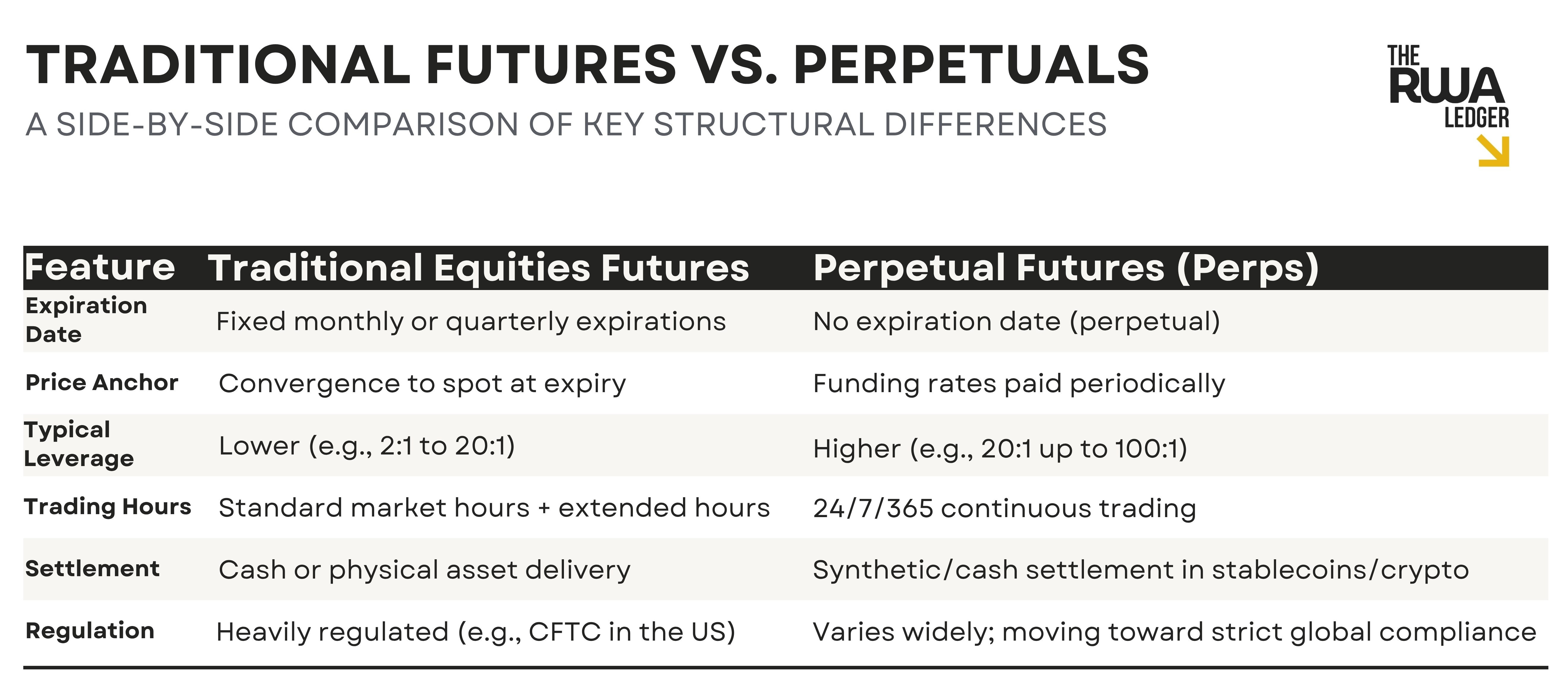

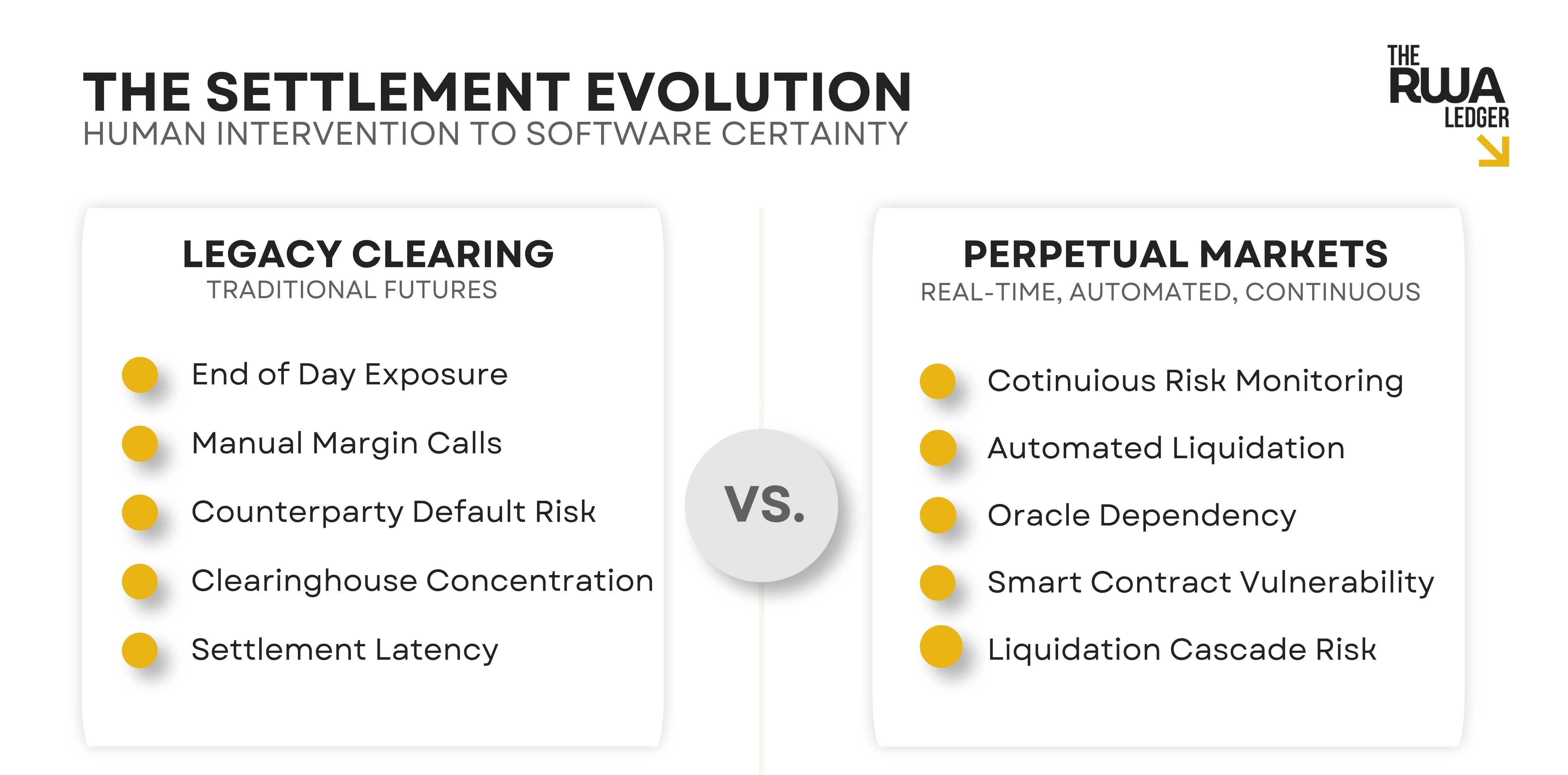

Core Mechanics: Traditional Futures vs. Perpetual Swaps

To understand how fundamentally this landscape has shifted, it is necessary to contrast the structural and operational mechanics that drive both ecosystems:

Legacy finance is no longer just observing an alternative asset class from a distance; it is witnessing a structural shift that challenges the necessity of the traditional futures timeline itself.

The Institutional Playbook: A Familiar Genesis

During the structural transition moving from the late 1990s into the corporate boom of the aughts, when I was working in corporate and public finance, my team and I originated, conceptualized, and structured what we saw at the time as cutting edge equity and debt offerings. Sitting on the investment banking side of the team, we weren’t trying to invent exotic derivatives for their own sake. We were trying to solve practical corporate and municipal problems: reduce financing costs, hedge positions, preserve and build liquidity, and manage risk more efficiently. Our day-to-day work focused on originating the capital raises, concepting the transaction architecture, and finalizing the structure of the finance and legal packages for our key clients.

To balance the massive balance sheet exposures inherent in these multi-million-dollar structures, we worked directly alongside and with the derivatives desk part of our team. While my side focused on the primary deal mechanics, financing terms, and regulatory filings, the derivatives desk enabled the custom over-the-counter overlays. Together, we worked alongside to create bespoke equity collars, total return swaps, and highly tailored currency cross-swaps to insulate client positions and manage issuer risk.

These integrated corporate finance offerings allowed major institutions to hedge highly concentrated stock allocations, manage liquidity during mergers, and minimize immediate tax liabilities without moving the underlying spot market. When these complex frameworks began skyrocketing during this transition into the aughts, the mainstream market met them with intense hesitation. Public commentators often labeled them as opaque, volatile, or structurally dangerous. Yet, behind closed doors, major investment banks and sophisticated asset managers aggressively adopted them because they offered an undeniable structural architecture that allowed large pools of capital to navigate around the rigid liquidity constraints of the spot market.

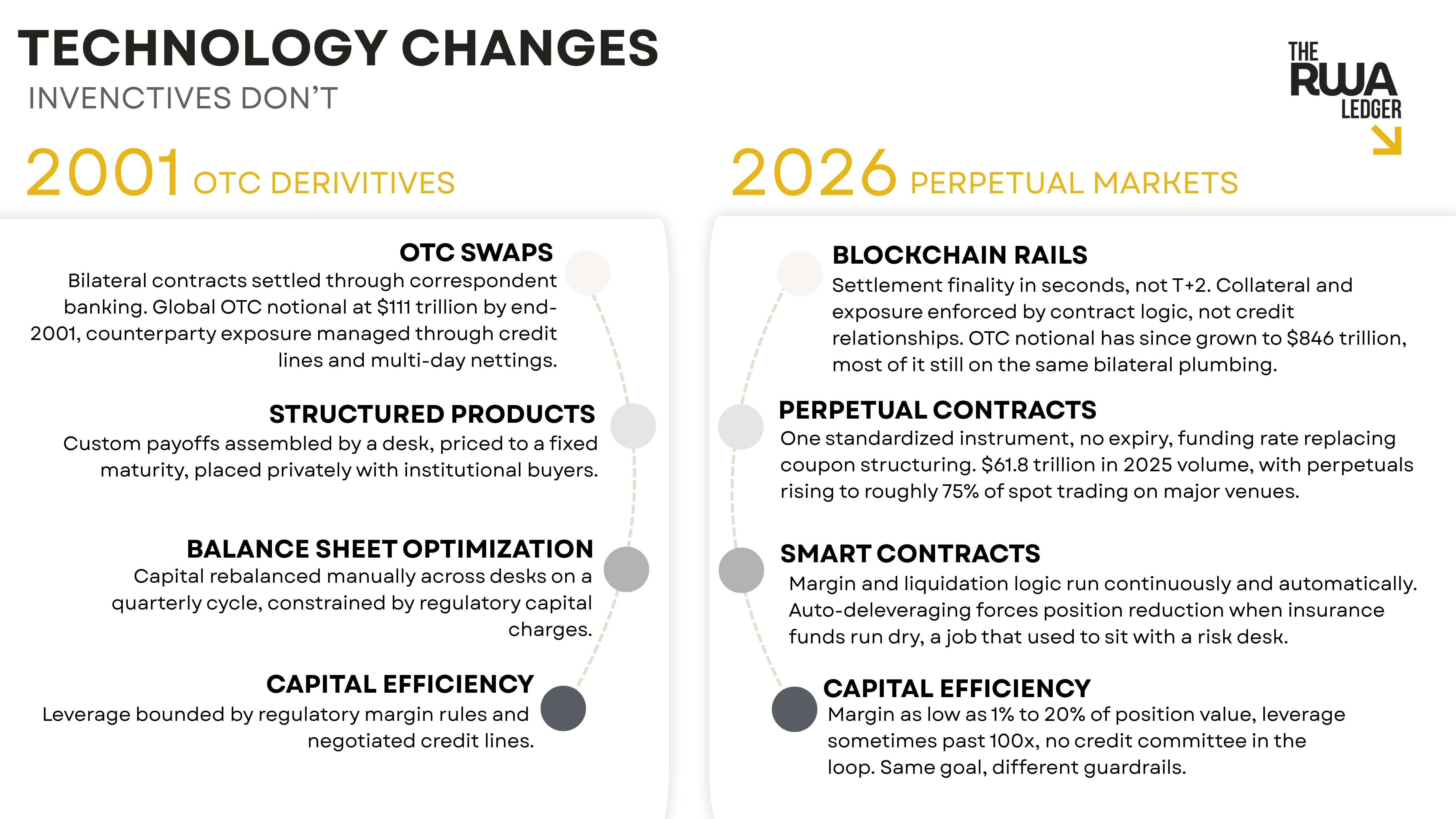

The Incentives Never Changed - Only The Infrastructure.

Twenty-five years ago, those exact same institutional incentives produced customized over-the-counter structures because they reduced structural drag, optimized capital efficiency, and solved pressing treasury constraints. Today, those identical economic drivers are steering modern asset managers toward perpetual swap infrastructure.

The technological rail has evolved from negotiated OTC contracts to cryptographic ledgers. This immutable, decentralized database programmatically verifies and records transactions without relying on an intermediary trust layer, but the institutional migration toward structural capital efficiency remains exactly the same. Capital allocators do not shift strategies because they are enamored by new technology; they shift because the new architecture fundamentally lowers the cost of maintaining a directional position. Different math, same economics.

The rails have changed. The motivations have not.

The Perpetual Shift

The concept of eliminating this temporal restriction began when Nobel laureate Robert Shiller penned a 1992 discussion paper proposing “perpetual claims on cash flows” to settle real estate and macroeconomic indexes [¹]. While Shiller envisioned these instruments as stabilizing forces for illiquid macro markets [²], the financial engineering community eventually adapted the design, transforming it into a highly liquid crypto derivative. Today, the perpetual swap has matured into a disruptive innovation in modern market structure.

Traditional futures assume humans intervene.

Perpetuals assume software intervenes.

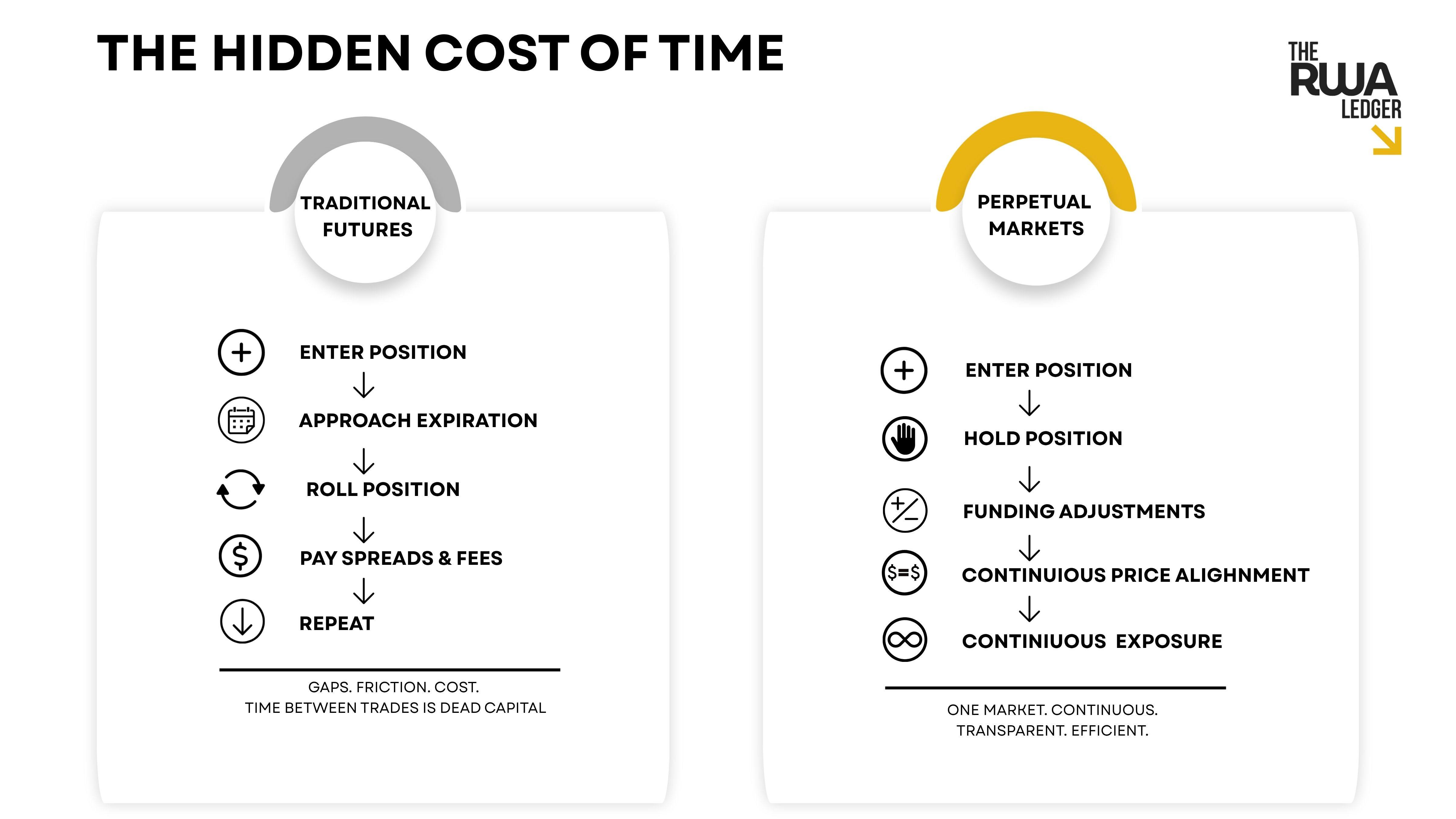

In financial markets, time is a structural tax. For decades, traders have accepted the roll as a mandatory cost of business, manually closing out positions to reopen them in the next calendar window. This incurs a constant slippage tax, compounded execution fees, and fragmented liquidity split across separate monthly pools.

Perpetual futures solve this architectural flaw by severing the link between time and settlement. Because perps never expire, a trader can hold a leveraged position indefinitely. Instead of an expiration date forcing price convergence to the spot market, perps utilize a dynamic funding rate. Paid periodically between long and short traders, funding rates act as an invisible gravity well, creating an immediate economic incentive for traders to pull the price back to par [³]. Rather than fragmenting into separate monthly expiration pools, liquidity compounds continuously within a single, unified order book.

The Settlement Equation

To grasp why institutional capital is migrating to this structure, we must strip away the secondary plumbing and look at how both systems handle risk during periods of extreme volatility. The core difference is not leverage; it is the method of systemic containment.

Traditional futures clearinghouses rely on an end-of-day clock. When a violent market downturn hits an account, the system relies on manual margin calls and 24-to-48-hour grace periods for human operators to settle the deficit. If an unprecedented macro event gaps an asset price down overnight, an entire account can drop into negative equity before the market even opens, creating counterparty defaults that threaten the broader clearing ecosystem.

The perpetual framework reduces this timeline vulnerability differently by replacing human settlement buffers with programmatic real-time autonomy. Operating continuously, the underlying code evaluates account health on a block-by-block basis using real-time price feeds. The moment an account crosses its safety threshold, the software instantly intervenes, liquidating the position in real time to ensure a default remains entirely localized to the individual losing participant.

To understand how aggressively this model is expanding, one only needs to look at the global volume ranges. Annual global crypto derivatives volume, anchored almost entirely by perps, regularly fluctuates within a massive $80 trillion to $90 trillion range [⁴]. On-chain trading venues are no longer niche experiments; the decentralized perp protocol Hyperliquid recently established a baseline range of $8 billion to $11 billion in total open interest [⁵], with a substantial portion now tied entirely to synthetic equities, commodities, and pre-IPO tech giants.

The institutional picture changed materially in 2026. Following a series of coordinated framework approvals from the Commodity Futures Trading Commission (CFTC), the structural barriers preventing the onshoring of perps officially collapsed [⁶]. An important inflection point arrived in mid-2026 when Kraken Pro brought onshore a comprehensive suite of CFTC-regulated perpetual futures via its Bitnomial acquisition [¹³, ⁷]. This allows U.S. large-scale capital allocators to deploy complex basis trading and hedging strategies inside a verified, domestic legal perimeter [¹³].

Case Studies in Extremes

The SpaceX IPO and The 24/7 Nasdaq

The theoretical efficiency of this programmatic system became a reality during a historic SpaceX initial public offering on the Nasdaq [⁸]. Synthetic pre-IPO perpetual futures allowed global traders to speculatively price SpaceX 24/7 before it ever hit a public order book. When SpaceX officially debuted on the Nasdaq, the perp contract surged to $176 prior to stock opening, marking a 30.37% premium over the initial $135 IPO floor. Trading on Hyperliquid reached $1.4 billion on debut day alone [⁵], while Binance’s contract eclipsed $5.6 billion within 24 hours. Data from Talos reveals that nearly half of all S&P 500 perpetual volume and more than 60% of oil perpetual volume on modern decentralized rails occurs outside of standard U.S. market hours [⁹].

The Drift Protocol Exploit on Solana

However, code-driven execution cut both ways during the catastrophic $285 million Drift Protocol exploit on Solana [¹⁰]. Moving risk execution down to atomic block times eliminates settlement latency but concentrates vulnerability. Attackers compromised trusted platform signers via a social engineering exploit that bypassed standard transaction expiration filters [¹¹]. Once inside, the hackers fabricated unbacked collateral assets, manipulated the protocol’s distributed oracles to validate their valuation, and systematically drained $285 million from the system’s vaults within 12 minutes [¹², ¹⁰]. The primary lesson is that software systems fail differently than human systems. Perps erase settlement drag, but they compress the timeline of failure, transforming a multi-day default into an instantaneous, irreversible loss of capital. [1]

Systemic Risks & Regulatory Safeguards

Innovation always uncovers new variations of old structural vulnerabilities. To believe that automated liquidation engines render the perp market immune to systemic failure is an illusion. In fact, looking back at the emergence of hyper-leveraged structures during the transition to the corporate boom of the aughts leading up to the great financial cracks of that decade reveals critical warnings.

During this structural shift, the rapid acceleration of complex, over-the-counter equity derivatives and customized credit default swaps acted as an untamed accelerant for market over-extension. High structural leverage allowed institutions to paint a false picture of underlying market liquidity. When macro factors shifted, the forced, systemic unwinding of those interconnected derivative positions exacerbated sharp asset contractions, dragging the broader spot markets down in non-linear cascades.

Perps do not exempt us from these market physics. They simply speed them up. The structural threats specific to the perpetual market include:

Liquidation Cascades: Because perps rely on continuous, real-time programmatic liquidations rather than human End-of-Day grace periods, they are highly prone to flash crashes. A sharp price drop triggers an auto-liquidation, which forces an automated market sell order, driving the price down further and instantly tripping the liquidation of the next trader.

Oracle Manipulation: Perps track an index value fed by distributed networks. If a malicious actor successfully compromises or manipulates an underlying spot price feed even for a few seconds, the automated system can trigger erroneous liquidations across completely innocent accounts [⁶].

The Funding Drag: For longer-term position holders, funding rates represent an invisible leak. In a strongly trending market, the cost of paying a continuous funding rate to maintain a position can quickly eat away a trader’s margin, pushing them closer to an automated liquidation threshold.

The Perpetual Paradigm

Every generation of financial infrastructure has attempted to remove a source of friction. Telegraphs replaced messengers, electronic exchanges replaced trading pits, and algorithmic execution compressed milliseconds into competitive advantages. Perpetual futures belong in that exact lineage. Their innovation is not leverage itself; it is the removal of time as an operational constraint.

This transition to a perpetual market structure affects every facet of the financial ecosystem differently:

Enterprise Investment Bankers: Structured debt or corporate finance offerings can increasingly rely on 24/7 tokenized perpetual layers instead of over-the-counter investment banking swaps, drastically compressing issuing friction and structural costs.

Institutional Asset Managers: Large-scale allocators must prepare for non-linear risk. Automated liquidation rules mean risk management desks cannot rely on traditional relationship lending buffers or overnight grace periods.

Compliance & Legal Teams: General counsel and compliance officers must pivot from retroactive, end-of-day auditing to real-time risk monitoring. Legal parameters must accommodate instantaneous, block-by-block programmatic contract liquidations, requiring continuous on-chain monitoring and oracle auditing.

Exchange Operators & Clearing Houses: Traditional legacy clearing houses face a massive competitive threat. To protect their market share, traditional clearinghouses must adapt by building their own continuous-settlement rails and hybrid multi-asset collateral engines.

Financial Regulators: The CFTC’s onshore push marks a shift from prohibition to systemic oversight [⁶]. Regulators must now intensely focus on setting standardized safety caps on leverage, monitoring oracle feed robustness, and ensuring decentralized insurance funds are capitalized enough to absorb localized shocks.

Conclusion

The structural evolution of the financial markets is accelerating toward continuous automation, and the traditional calendar-bound contract is the first major casualty. By systematically dismantling the operational taxes of manual contract rollovers, perps have unlocked an environment where liquidity never fragments; it compounds. Simultaneously, the transition from the slow, human-intervened timelines of end-of-day clearinghouse margin calls to automated, second-by-second liquidation engines has removed structural credit risk from the clearing equation.

Whether that migration occurs over five years or fifteen, history suggests that capital eventually follows efficiency. However, as the jarring lessons of the early aughts derivative excesses and the modern Drift Protocol exploit vividly demonstrate, automation does not eliminate human failure or systemic risk [⁶]. It simply alters the landscape of how vulnerability expresses itself. Continued understanding, bulletproof smart contract security, and rigorous regulatory oversight are not roadblocks to growth. They are the vital, non-negotiable pillars required to build a functional, efficient, and permanent marketplace.

Whether perpetual futures ultimately become the dominant market structure is still an open question. The direction of travel, however, is becoming increasingly clear. Markets have always rewarded mechanisms that reduce friction, improve liquidity, and deploy capital more efficiently. Perpetuals are the latest, and perhaps most consequential, expression of that principle.

The boundaries between crypto derivatives and capital markets are fading. In their place stands a unified, 24/7, programmatic marketplace where capital moves at the speed of code, and the trading calendar is permanently dead.

The future of futures may be the absence of expiration.

Primary Source References

Shiller, Robert J. (1992). “Measuring Asset Values for Cash Settlement in Derivative Markets: Hedonic Repeated Measures Indices and Perpetual Futures.” Cowles Foundation Discussion Paper No. 1036. Yale University. (Alternative digital compilation available via the institutional Yale EliScholar Repository).

Shiller, Robert J. (1993). “Aggregate Income Risks and Hedging Mechanisms.” National Bureau of Economic Research (NBER) Working Paper Series, W4396. (Official listing hosted on the NBER Papers Registry).

Bajaj Finserv Asset Operations. (2025). “How Perpetual Contracts Automate Continuous Price Alignment to Spot Indexing.” Core Financial Lexicon Core Infrastructure.

CoinGlass Analytics. (2025). “Crypto Derivatives Volume Hits $86 Trillion in 2025, Liquidations Top $150B.” Institutional Market Review Series. (Annualized framework metrics compiled under the CCData Exchange Intelligence Reports Archive and summarized via TradingView Institutional Volume Data).

Hyperliquid Protocol Lab. (2026). “On-Chain Open Interest Baseline Metrics and Asset Allocation Tranches.” Hyperliquid Layer-1 Native Disclosures. (Live chain analytics tracked via DefiLlama Hyperliquid Dashboard).

Commodity Futures Trading Commission (CFTC). (2026). “Strategic Framework Approvals for Onshore Derivatives Clearances and Oversight Shifts.” Official Federal Register & Speeches Portal. (Contextual reporting available through Markets Media Intelligence).

Kraken Pro Corporate. (2026). “Launch Parameters of CFTC-Regulated Onshore Pipelines for Domestic Capital Allocators.” Payward / Bitnomial Regulatory Fact Sheets. (Corporate disclosure distributed via Business Wire Corporate Newsroom).

Nasdaq Global Newsroom. (2026). “SpaceX Goes Public: SPCX Now Available to Trade Following Historic Nasdaq Debut.” Corporate Issuance Data. (Underwriting capital allocations and Form S-1 breakdown details are preserved via the BitMEX Underwriting Analysis Journal and tracked live via CNBC Market Intelligence).

Talos Global Trading Insights. (2025). “February 2026 Market Update: Crypto Caught Between Gold & Growth” Talos Market Intel Journal. (Ongoing institutional reports, macro execution risk tracking, and market structure insights are updated directly via the Talos Insights Infrastructure Registry and reported via Crowdfund Insider Market Analytics).

Elliptic Crypto Forensics. (2026). “On-Chain Post-Mortem of the Drift Vault Exploit and Systemic Capital Draining.” Elliptic Forensic Ledger.

Chainalysis Cyber Intelligence. (2026). “The Drift Protocol Hack: How Privileged Access Led to a $285 Million Loss” Chainalysis Incident Report. (Further operational reporting details are preserved on the BlockEden Drift Recovery Register).

TRM Labs (2026). “North Korean Hackers Attack Drift Protocol In USD 285 Million Heist.”

Bitnomial Exchange Infrastructure Group. (2025). “The First U.S. Perpetual Futures.” Bitnomial Market Operations Thought Leadership Series. (Live engine specifications and margin pool data are tracked continuously via the Bitnomial Perpetual Futures Markets Hub).