On The Ledger |No. 002: Eighteen months of lobbying, legislation, closed rooms, and then a shareholder letter.

A reading of the letter, the week that followed, and the fight that preceded it.

Reading: Jamie Dimon’s 2025 Annual Letter to Shareholders, JPMorganChase -April 6th, 2026, and the week that followed.

The Letter

Every year, Jamie Dimon writes his annual letter to shareholders, and each time, the questions that come to mind are similar: what is the letter really saying, and what might it be softening or excluding?

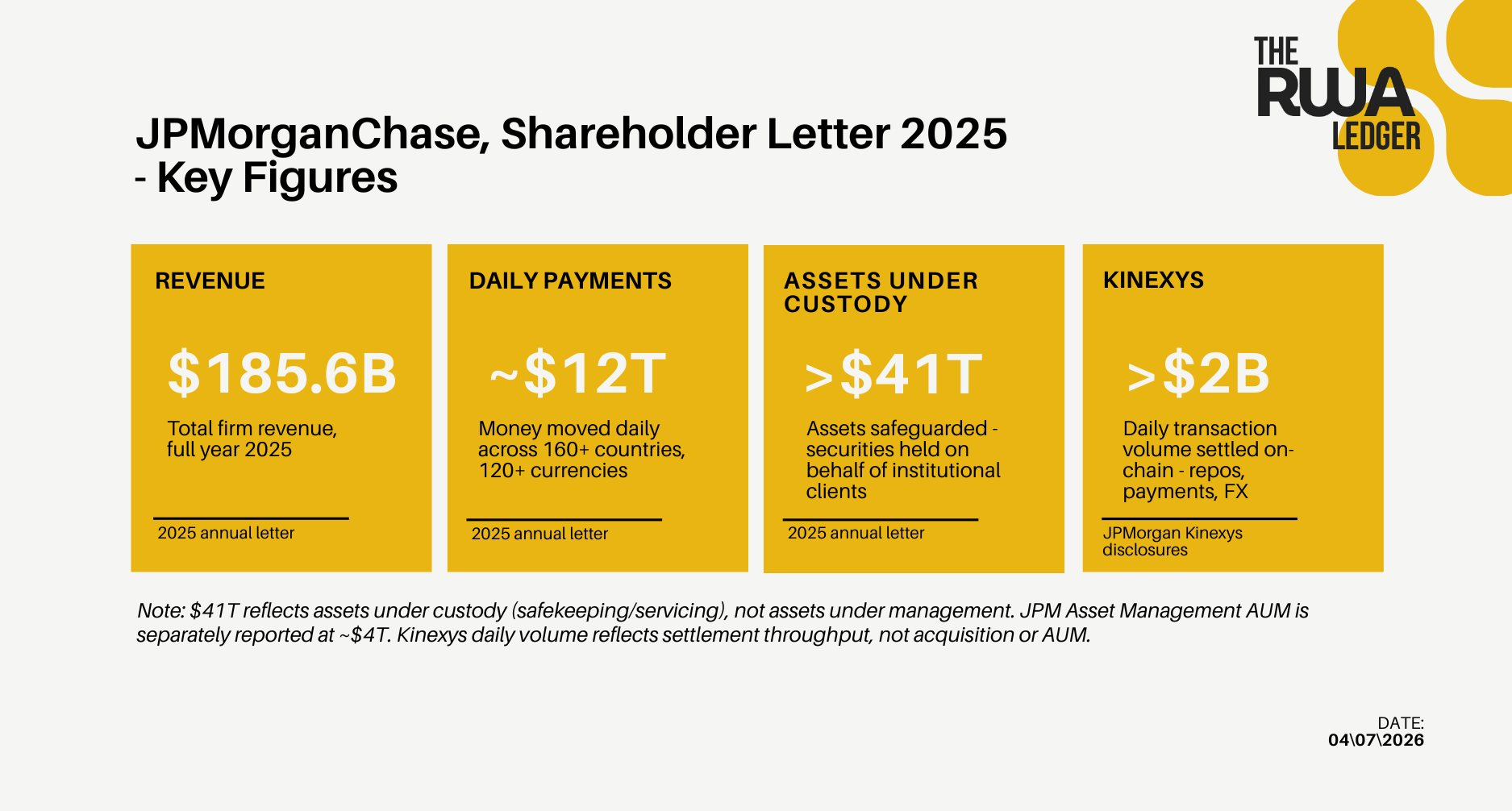

This year’s letter, published on April 6th, spans 48 pages. Most of it concentrates on key risks: the war in Iran, inflation, private credit, and AI. While these points are largely accurate, it’s important to note that they are also the topics Dimon is most comfortable discussing openly.

Start with the economy. Dimon calls it resilient. Read the letter closely, and you find the qualifier he buries in the same sentence: “consumers still earning and spending, (though with some recent weakening).”[1] Credit card balances now sit above $1.3 trillion. Delinquencies are rising. Consumer spending is increasingly supported by credit rather than income growth. Resilience is the word you use to describe forward momentum without inviting questions about what lies beneath it.

On inflation, he is more candid. He calls it the “skunk at the party,” and the framing is precise: the war in Iran creates conditions for persistent oil and commodity price shocks that could push rates higher than markets currently expect.[2] He adds that “interest rates are like gravity to almost all asset prices.”[1] That is not a hedge. That is a warning about the repricing risk embedded in the current consensus.

On private credit, the letter says the $1.8 trillion market “probably” does not present systemic risk, then spends several paragraphs describing weakening credit standards, opaque valuations, and losses already running higher than the environment should produce.[1] Probably is doing a lot of work in that sentence, and it is worth asking why a CEO with this much visibility into the credit system reaches for that word rather than a stronger one.

On AI, there is no hedging. He calls it transformational and says the pace will exceed prior technological revolutions. JPMorgan has a $19.8 billion technology budget for 2026, with AI at the center. Reports published the week following the letter confirm Dimon is expected to step down within 24 months, with Marianne Lake and Troy Rohrbaugh emerging as frontrunners to succeed him.[3] A CEO setting a technology agenda of that scale eighteen months before a handover is making a statement about what he wants the institution to become, not just what it is.

Then there is the blockchain passage. It occupies one paragraph in a 48-page document. Most coverage treated it as a footnote. Here is what it says:

“A whole new set of competitors is emerging based on blockchain, which includes stablecoins, smart contracts, and other forms of tokenization.”— Jamie Dimon, 2025 Annual Letter to Shareholders, JPMorganChase

To understand why that paragraph carries more weight than its length suggests, you need the eighteen months that preceded it.

The Arc

Here is the short version of what happened, and why it matters.

The crypto industry spent nearly $250 million backing candidates ahead of the 2024 election, with Coinbase and a16z crypto as the two most powerful voices.[4] That investment produced real wins, including the passage of the GENIUS Act last summer, which established a federal framework for payment stablecoins. But it also produced something the industry did not fully anticipate: it brought the banking lobby into the fight in a way it had not been before.

The specific issue was yield. A structural feature of the GENIUS Act allowed stablecoin issuers’ partners to pay yield on stablecoin holdings even as issuers themselves were restricted. Coinbase, through its revenue-sharing arrangement with Circle on USDC, was offering holders approximately 3.5% annually. For context, the FDIC national average savings account rate is 0.39% APY as of April 2026, while the best high-yield savings accounts offered by online banks reach approximately 4.0% to 4.1% APY.[5] Stablecoins are not FDIC-insured, a distinction the banking industry has consistently raised as a consumer-protection concern, and regulators have not yet resolved it through a unified framework. The yield differential relative to the national average is significant; relative to the best available high-yield savings products, it is narrower, and that distinction matters for how deposit flight risk is actually modeled.

The deposit flight concern is worth pausing on because it is the empirical foundation on which the entire banking industry argument rests, and it is now contested. Two figures circulate in the debate, and they are measuring different things. The $6.6 trillion figure, cited by bank executives and drawn from a Treasury analysis, models long-term deposit migration across the entire U.S. deposit base under aggressive stablecoin adoption scenarios, with no specified time horizon.[6] The $1.3 trillion figure comes from the Independent Community Bankers of America and represents their estimate of near-term deposit losses specifically at community banks, a narrower institutional subset, with $850 billion in reduced lending to follow.[7] These are not competing estimates of the same thing. They are different models, different scopes, and different timeframes, which is precisely why the debate has been difficult to resolve at the legislative level.

A White House Council of Economic Advisers report published April 8th took a narrower view of both: eliminating stablecoin yield, in their base case, lifts bank lending by approximately $2.1 billion, roughly 0.02% of total loans, while imposing a net welfare cost on consumers.[7] The CEA's reasoning is that most stablecoin reserves remain within the banking system, recycled into Treasuries or other deposits, thereby limiting the extent of real balance-sheet flight. By their estimate, only approximately 12% of reserves are effectively locked out of lending.

Deposit flight - Competing Estimates

Banking industry position

$6.6T in potential deposit migration modeled across the entire U.S. deposit base under aggressive long-term adoption scenarios (Treasury analysis, no specified time horizon). ICBA separately estimates $1.3T in near-term losses for community banks, specifically $850B in reduced lending. Senior executives at JPMorgan and Bank of America argue that stablecoin yields, without bank-equivalent regulation and FDIC insurance requirements, create an uneven playing field and systemic deposit risk.

White House CEA position

Eliminating stablecoin yield lifts bank lending by ~$2.1B, approximately 0.02% of total loans. Most stablecoin reserves recycle within the banking system via Treasuries and deposits, limiting real balance-sheet flight to approximately 12% of reserves. A yield prohibition imposes net welfare costs on consumers with minimal benefit from lending. Stablecoin balances are structurally distinct from bank deposits and should not be regulated as equivalent.

The empirical gap between these positions has not been closed. What is clear is that the deposit flight question will shape how stablecoin yield is regulated for years, and the answer is being contested simultaneously in Congress, in regulatory filings, and in the White House's own economic analysis, as the legislation moves toward a vote. For anyone building, allocating, or advising in this space, that unresolved empirical uncertainty is itself a material consideration.

The CLARITY Act passed the House 294-134 in July 2025 with bipartisan support.[6] By the time it reached the Senate Banking Committee, the stablecoin yield question had become the load-bearing issue. The American Bankers Association made opposing yield-bearing stablecoins its primary policy priority. JPMorgan and its peers lobbied accordingly.

On January 14, 2026, hours before the Senate Banking Committee was scheduled to mark up the bill, Brian Armstrong, CEO of Coinbase, publicly posted that Coinbase could not support the legislation as written.[8] The committee postponed immediately. Stablecoin-related revenue represented approximately 20% of Coinbase's total revenue in the third quarter of 2025. That context is worth holding alongside Armstrong's stated objections about regulatory fairness.

Davos followed two weeks later. According to reporting from The Wall Street Journal,[9] Dimon interrupted a coffee meeting Armstrong was having with former UK Prime Minister Tony Blair, told Armstrong he was "full of s—," and objected to television appearances in which Armstrong had accused banks of working behind the scenes to undermine the legislation. Bank of America's Brian Moynihan told Armstrong that if Coinbase wanted to offer deposit-like products, it should be a bank. Wells Fargo's Charlie Scharf declined to engage. Citigroup's Jane Fraser, whose institution maintained an active banking relationship with Coinbase, gave him under a minute before the conversation ended.

The Davos confrontation made the conflict legible to a general audience. The conflict itself had been building for eighteen months.

In March, Dimon told CNBC that platforms paying yield on stablecoin balances should face bank-equivalent regulation: "If you are going to be holding balances and paying interest, that's a bank and you should be regulated as a bank."[10] The White House pushed back within 24 hours. Patrick Witt, executive director of the President's Council of Advisors for Digital Assets, wrote publicly that Dimon's framing was "deliberately inaccurate," arguing that the GENIUS Act already prohibits stablecoin issuers from lending reserves, which is what makes bank-level regulation appropriate for deposit-taking institutions, and that stablecoin balances should not be treated as equivalent to bank deposits.[11]

On March 20th, Senators Tillis and Alsobrooks announced an agreement in principle: passive stablecoin yield, earned simply for holding a dollar-pegged token, would be banned; activity-based rewards tied to payments and transactions would be permitted.[12] When draft text circulated among crypto industry leaders in closed-door Capitol Hill sessions days later, Circle fell 20% in a single session, wiping $5.6 billion in market value.[13]

Armstrong, whose January post withdrawing Coinbase's support had been enough to halt the Senate Banking Committee markup entirely, had not commented publicly on the March text.On April 1st, Coinbase's Chief Legal Officer, Paul Grewal, told Fox Business the stablecoin yield dispute was "very close to a deal," adding that there had been "no evidence of deposit flight whatsoever" to support the banking industry's core argument.[15] Nine days later, Armstrong reversed course entirely. Following a public statement from Treasury Secretary Scott Bessent urging Congress to act, Armstrong wrote: "We agree. Thank you Scott Bessent for saying it. It's time to pass the Clarity Act."[16] The silence had ended. Whether the deal it reflects holds through the markup is the remaining question.

The shareholder letter arrived on April 6th, the same week Armstrong reversed course, and Coinbase signaled it could accept the legislative framework the banking industry had largely shaped. In it, Dimon named tokenization a competitive threat alongside Block, Revolut, and Stripe. That framing matters because it is not the language of a bank exploring a new market. It is the language of a bank that has already been building in one.

Kinexys is JPMorgan’s blockchain-based payments and settlement platform, launched in 2020 as Onyx and rebranded in 2024. It enables near-instant fund transfers between institutional clients without relying on traditional intermediaries, settling transactions across currencies, time zones, and asset types in real time. It currently processes over $2 billion in daily transaction volume, is targeting $10 billion in daily transaction volume, and counts BlackRock, Siemens, Mitsubishi, and Qatar National Bank among its clients.[14] The platform is expanding into private credit and real estate tokenization. This is production infrastructure, not a proof of concept.

Read in that sequence, the shareholder letter is not the beginning of JPMorgan’s position on tokenization. It is its most formal and permanent expression, filed with shareholders, on the record, the week the regulatory fight it had been waging moved toward the outcome the banking industry sought.

What The Week Confirmed

The macro picture and the infrastructure story are connected in a way that most coverage missed.

If Dimon is right that inflation stays stickier than markets expect, the cost of capital for tokenization infrastructure builders increases alongside rates. If he is right that private credit standards have been quietly weakening, the assets most often cited as tokenization candidates, private credit instruments among them, become harder to originate and more complex to underwrite at scale. The letter’s cautious macro frame is not background noise for the blockchain passage. It is the operating environment in which that infrastructure will have to prove itself.

The CLARITY Act is not resolved. The Senate Banking Committee markup is targeted for the second half of April. Senator Bernie Moreno has stated that if the bill does not reach the Senate floor by May, crypto legislation risks going dark until after the midterm cycle.[12] Five sequential legislative hurdles remain. The debate over the deposit flight, now with competing empirical estimates from the banking industry and the White House’s own economists, will continue to frame those negotiations regardless of which number proves closer to reality.

What the week confirmed is something simpler…

The largest bank in the world has placed on record that “a whole new set of competitors is emerging based on blockchain, which includes stablecoins, smart contracts, and other forms of tokenization”[1] - and is building the rails to respond to that threat at scale.

The letter, the lobbying, and the Kinexys buildout are not separate activities. They are the same strategy, and shaping it.

That is worth understanding clearly, whatever you think of the outcome.

Sources

Complete footnotes [1]–[16]

[1] Jamie Dimon, 2025 Annual Letter to Shareholders — JPMorganChase, April 6, 2026

[2] Dimon warns Iran war may drive inflation and interest rates higher — Reuters, April 6, 2026

[4] Why Coinbase split with a16z on the CLARITY Act — Fortune, January 21, 2026

[8] Crypto bill on knife’s edge as Coinbase CEO objects — Fortune, January 14, 2026

[10] Dimon: crypto industry should be regulated like banks — DL News, March 3, 2026

[11] White House counters Dimon stablecoin yield logic — The Block, March 4, 2026

[12] CLARITY Act Unblocked: Stablecoin Yield Compromise Reached — Disruption Banking, March 22, 2026

[13] CLARITY Act: Banks Still Winning on Stablecoin Yield — FinTech Weekly, March 2026

[14] Dimon sees new competitors from blockchain, stablecoins — Cointelegraph, April 6, 2026

[15] Coinbase CLO Paul Grewal: CLARITY Act stablecoin yield deal “very close” — The Block, April 1, 2026. https://www.theblock.co/post/396170/coinbase-clo-grewal-clarity-act-very-close

[16] Coinbase CEO Armstrong backs CLARITY Act after Treasury Secretary Bessent call to act — GNCrypto citing Armstrong X post, April 10, 2026. https://www.gncrypto.news/news/coinbase-ceo-armstrong-backs-clarity-act-treasury-call-stablecoin-rules

Reference (observational, not primary): Jamie Dimon’s Annual Letter Is A Subtle Warning — QTR Fringe Finance, April 6, 2026

Nice overview of the blockchain angle within Morgan’s letter to shareholders and great insights into their future facing intentions in the market.