This article does not attempt to summarize every panel or presentation delivered at BTC Prague 2026. Instead, it seeks to identify the structural themes that emerged across the conference.

Introduction

Every major Bitcoin conference leaves behind a dominant narrative.

In 2021, it was institutional adoption.

In 2023, it was resilience in the aftermath of the market crashes.

In 2024, it was the institutionalization of Bitcoin through spot ETFs.

BTC Prague 2026 felt different.

Rather than converging around a single narrative, the conference revealed the simultaneous emergence of several distinct, increasingly interconnected visions of Bitcoin.

For some, Bitcoin remains a tool of sovereignty, self-custody and personal freedom.

For others, it is becoming a new form of digital capital capable of supporting credit markets, treasury strategies and institutional investment products.

For others still, Bitcoin represents a framework for resilience in an increasingly uncertain technological, geopolitical and monetary environment.

These visions are often presented as competing narratives because they were built for different users, at different scales, under different regulatory constraints. What BTC Prague 2026 suggested is that the ecosystem has grown large enough to hold all of them - and that participation can coexist simultaneously

The result is not a single story about Bitcoin, but a framework for understanding how different forms of participation are beginning to coexist within the same ecosystem. What follows maps the four themes that ran through the conference and what they mean.

I. Resilience: Designing for an Uncertain Future

One of the most striking themes emerging from BTC Prague 2026 was the growing importance of resilience. Not as a technical feature, but as a design principle. For most of Bitcoin’s history, the central question was whether the protocol itself would survive.

After more than fifteen years of operation, that question appears largely settled.

The more relevant question today is different:

How do we build systems, institutions, and financial infrastructure capable of surviving the uncertainties surrounding Bitcoin’s future?

One of the conference’s most thought-provoking sessions addressed a subject often discussed through sensational headlines but rarely through a rigorous risk-management lens: quantum computing. Fred King, founder of CryptoSnake, explored the relationship between quantum computing and Bitcoin through the lens of Quantum vs. Bitcoin: Three Possible Futures.

His presentation explored the quantum threat through three broad scenarios, reflecting different assumptions about technological progress, migration timelines, and the ability of digital infrastructures to adapt.

The Optimistic Case: Quantum Stays a Distant Threat

Under this scenario, practical quantum computing remains sufficiently distant to give Bitcoin and other digital infrastructures ample time to prepare, upgrade, and migrate toward quantum-resistant cryptographic standards.

The Moderate-Impact Case: Disruption Arrives, But With Warning

This scenario envisions meaningful advances in quantum capabilities emerging within a timeframe that requires active preparation, while still providing institutions, developers and network participants with an opportunity to respond and adapt.

The Critical-Threat Case: The Math Moves Faster Than the Network

The most challenging scenario is that quantum capabilities advance faster than expected, placing increasing pressure on existing cryptographic assumptions and on the ability of digital infrastructures to coordinate an effective response.

In doing so, King challenged the common assumption that the emergence of powerful quantum computers would inevitably trigger a sudden Bitcoin apocalypse. The central question, he argued, is not whether quantum computing could eventually challenge existing cryptographic assumptions. The question is whether decentralized systems can adapt before that moment arrives.

Perhaps the most important observation of the session was that the challenge extends far beyond cryptography itself.

As King noted:

“The challenge isn’t just the math. It is the social layer.”

Even if viable post-quantum solutions exist, decentralized networks must still coordinate migration paths, establish incentives, reach consensus, and maintain trust throughout the transition. The defining challenge is therefore not technological innovation alone. It is the ability of decentralized systems to coordinate collective adaptation under uncertainty. Proposed post-quantum migration pathways are being discussed and tested within the Bitcoin ecosystem, indicating that the debate has moved beyond awareness and into preparation.

King also emphasized that Bitcoin is not uniquely exposed to this challenge. Governments, banks, payment networks, and critical digital infrastructures all rely extensively on cryptographic systems that could eventually require post-quantum upgrades.

In that sense, Bitcoin is not an exception. It is part of a much broader technological transition.

Only two days before BTC Prague, remarkably similar questions were being explored at the Q-Day Summit in Paris during a panel discussion titled “Quantum Computing, Blockchains and On-Chain Finance in a Post-Quantum World,” which I had the opportunity to moderate. The panel brought together Professor Jean-Jacques Quisquater, one of Europe’s leading cryptographers, Thibault Verbiest, a pioneer of digital asset law in Europe, Manu Nalepa, Ethereum Core Developer, Noé Curtz, Deputy CTO and specialist in digital infrastructure architecture, and Yacine Wayne, CEO of Quantos, a blockchain infrastructure designed with post-quantum resilience in mind.

The Author, Ruben Landsberger, moderated a panel discussion called “Quantum Computing, Blockchains and On-Chain Finance in a Post-Quantum World” at Q-Day Summit

Together, cryptographers, blockchain researchers, cybersecurity specialists and digital asset practitioners examined the implications of post-quantum cryptography for digital signatures, financial infrastructures and long-term asset security. What emerged from both events was a strikingly similar conclusion: the defining challenge is not the pace of quantum development itself, but whether institutions can adapt before that development forces their hand.

Quantum computing remains a challenge that requires preparation, not panic.

The objective is not to predict a single future, but to build systems capable of adapting to multiple possible futures, shifting the focus away from quantum computing itself and toward a more fundamental question of institutional readiness.

Institutional readiness, in this context, means five things simultaneously: protocol resilience, custody resilience, operational resilience, regulatory resilience and portfolio resilience.

From this lens, quantum computing functions less as a prediction than as a stress test, forcing organizations to examine whether their systems, governance structures and decision-making processes can adapt to technological change whose timing, scale and ultimate impact remain uncertain. The significance of the quantum debate extends beyond cryptography because it illustrates a broader shift in how resilience is understood: not predicting a single future correctly, but preserving the ability to adapt across multiple possible futures simultaneously.

For asset managers, custodians and infrastructure providers, the challenge is no longer simply securing Bitcoin today. It is building structures capable of adapting to technological, regulatory and geopolitical changes over decades.

In that sense, the institutions building Bitcoin infrastructure today are making long-term bets not merely on Bitcoin itself, but on the resilience of the architectures surrounding it.

And resilience, more than certainty, may prove to be one of Bitcoin’s most valuable attributes.

If resilience is about designing systems that survive uncertainty, sovereignty is about deciding who controls them, and was perhaps the most emotionally resonant theme at BTC Prague 2026. And the most frequently misunderstood outside the Bitcoin ecosystem. Sovereignty, in this context, is an operational concept rather than a political statement. And at BTC Prague 2026, it was defined more broadly than is often assumed.

Sovereignty is often reduced to self-custody. BTC Prague 2026 suggested a broader interpretation.

Sovereignty is not merely about controlling private keys. It is about preserving the ability to make meaningful decisions regarding one’s assets, identity, mobility, and long-term wealth — without requiring permission from any single intermediary, institution, or jurisdiction.

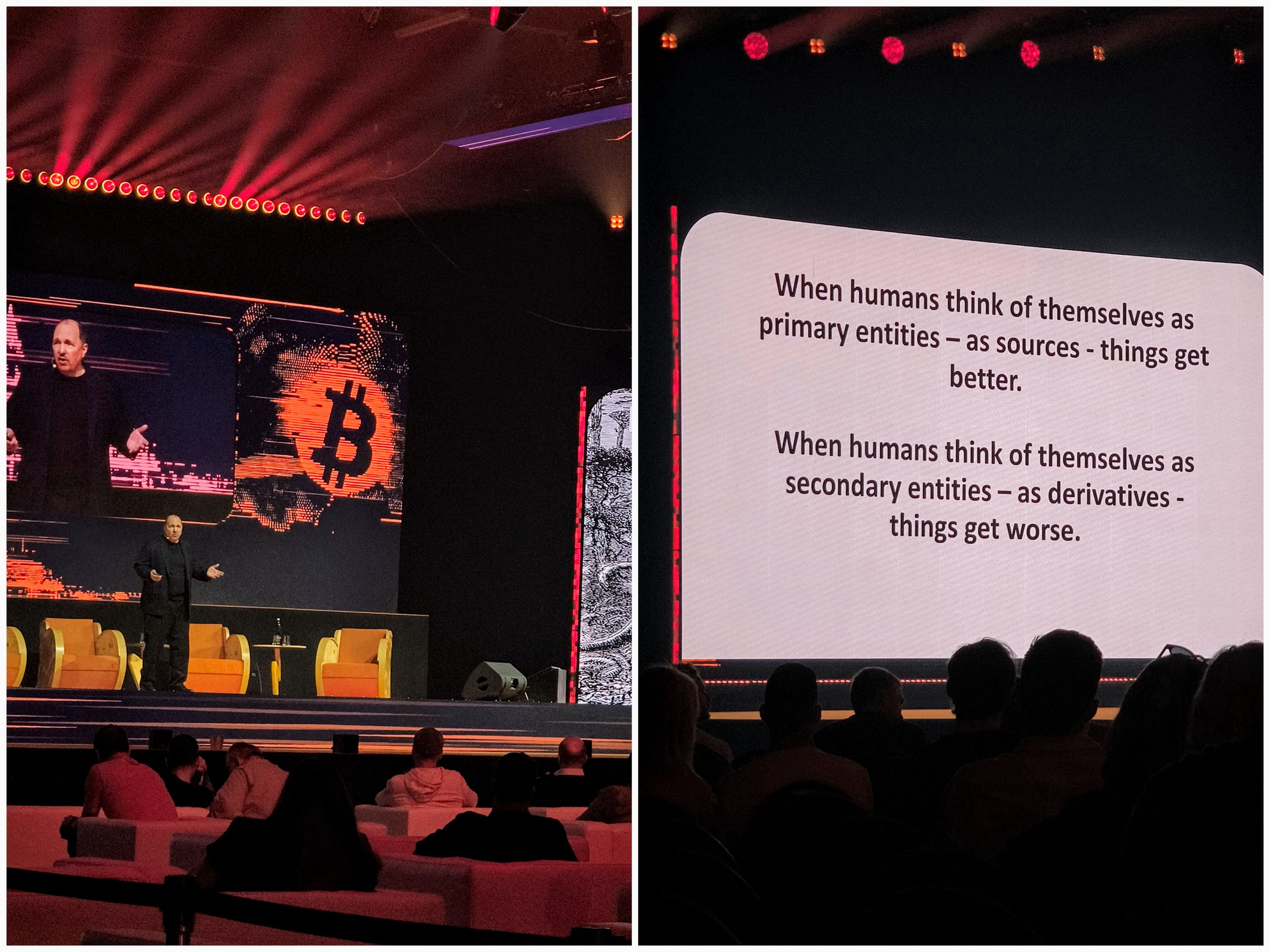

At BTC Prague 2026, Paul Rosenberg — Cypherpunk author and founder of Cryptohippie — offered a perspective that extended this concept beyond its financial dimensions.

His keynote, Bitcoin Is Still Bigger Than You Think It Is, argued that Bitcoin’s significance cannot be reduced to price appreciation or technological innovation.

Bitcoin, in his framing, reflects a broader shift in how individuals relate to money, institutions, and decision-making.

Monetary systems, he argued, implicitly encode assumptions about who acts and who is acted upon. Systems built around centralized issuance and hierarchical control tend to treat individuals as secondary participants within a larger structure — recipients of decisions made elsewhere.

Bitcoin, by contrast, is designed around the premise that individuals are primary actors: capable of holding, transferring, and preserving value without requiring prior authorization from any intermediary.

Paul Rosenberg’s Keynote, “Bitcoin Is Still Bigger Than You Think It Is” at BTC Prague 2026

As Rosenberg put it on one of his slides:

“When humans think of themselves as primary entities — as sources — things get better.

When humans think of themselves as secondary entities — as derivatives — things get worse.”

For an institutional audience, this may initially sound like ideology. Yet beneath the philosophical language lies a practical observation about incentives, responsibility, and the distribution of decision-making power within systems.

It is not merely philosophy. It is architecture.

The same logic that Rosenberg applied to individuals can be applied directly to institutions navigating an increasingly complex regulatory, technological, and monetary environment: the question is not simply what assets to hold, but what structures preserve the ability to act as an originating decision-maker rather than a dependent participant.

Sovereignty, in this sense, is not exclusively a Bitcoin principle. It is an organizational design principle.

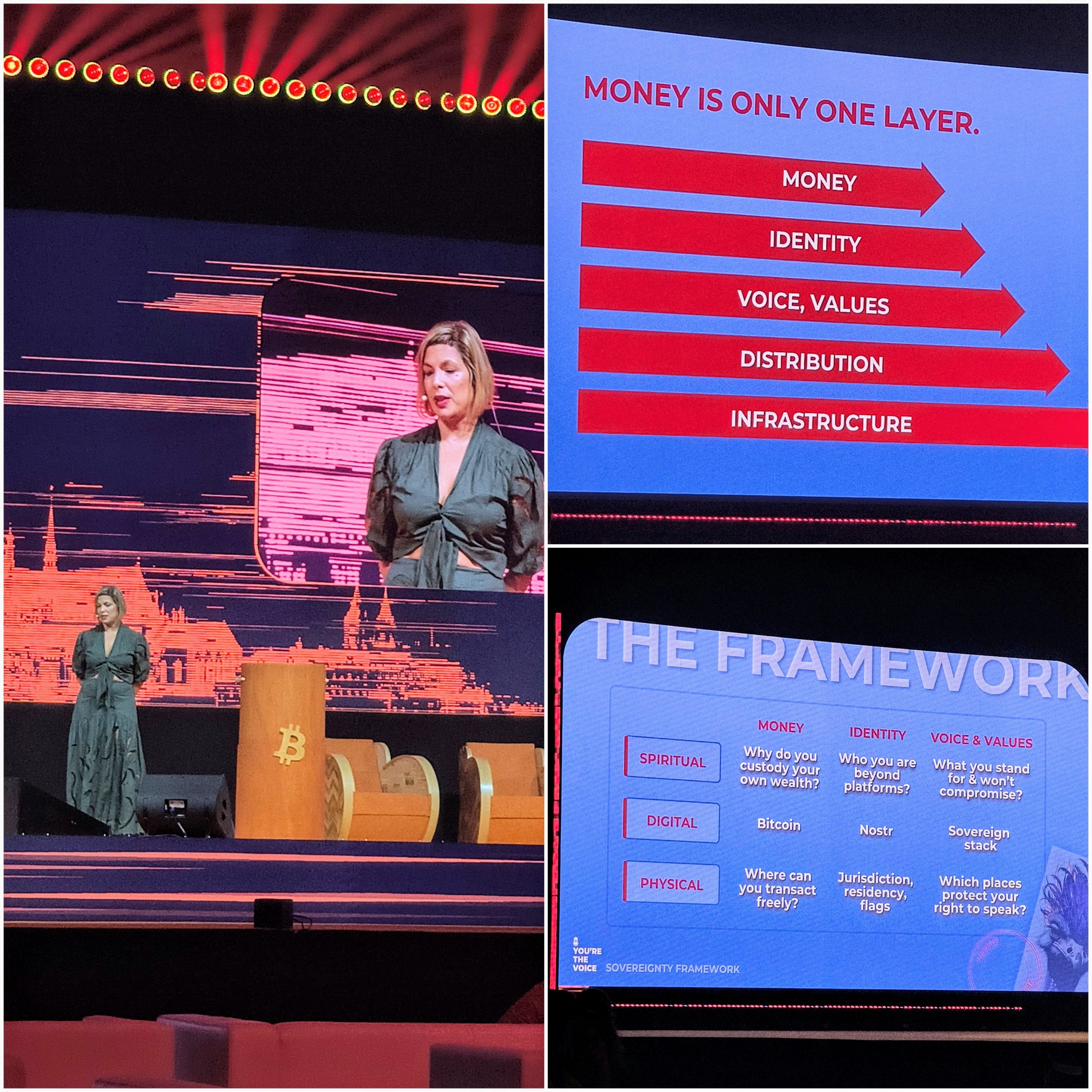

Efrat Fenigson’s session, The Digital Sovereign Individual, extended this concept beyond financial assets. Drawing on her own experiences of deplatforming, censorship, and cross-border Bitcoin usage, she argued that self-custody of money is only one dimension of sovereignty.

Her central observation was simple: most people who practice Bitcoin self-custody still do not control their identity, audience, or voice.

Sovereignty, in her framing, is not a single layer. It is a stack.

Financial sovereignty — the ability to hold and transfer value without permission — is one dimension. But in an increasingly digital world, identity systems have become a parallel control point: determining access to financial services, digital platforms, professional opportunities, and cross-border mobility.

In a digital economy, controlling identity credentials may become as strategically important as controlling financial assets.

Efrat Fenigson’s session on The Digital Sovereign Individual at BTC Prague 2026

This question is no longer theoretical. In Europe, the eIDAS 2.0 framework is laying the foundations for the European Digital Identity Wallet (EUDI Wallet), with member states expected to make digital identity wallets available to citizens and residents by the end of 2026. (See Regulation (EU) 2024/1183 establishing the European Digital Identity Framework : https://eur-lex.europa.eu/eli/reg/2024/1183/oj)

The objective is to enable individuals and organizations to hold and selectively share verified credentials across jurisdictions. As digital identity infrastructure becomes embedded in financial services, access management and regulatory compliance, questions of control, portability and governance become increasingly strategic.

For institutional readers, this observation carries a direct operational implication. As digital identity frameworks emerge across jurisdictions — through eIDAS 2.0 in Europe and digital ID initiatives elsewhere — the question of who controls identity infrastructure is becoming as relevant to compliance, KYC and client onboarding as the question of who controls custody infrastructure.

Sovereignty, whether individual or institutional, increasingly means preserving decision-making power across multiple interconnected layers simultaneously.

This has direct operational implications.

Whether the holder is an individual or a pension fund, the core questions of Bitcoin custody remain structurally identical:

Who ultimately controls the keys? What happens to assets in the event of custodian insolvency? How does the applicable legal framework define ownership of digital assets?

These are due diligence questions, and they apply at every scale of the Bitcoin ecosystem. Ultimately, sovereignty is less about the specific tools chosen and more about preserving the capacity to act as an originating decision-maker rather than as a dependent participant; once preserved, it expands what is possible.

Most financial systems offer choices, but they are designed to reserve the right to revoke them. What sovereignty actually preserves is not the existence of those choices but their durability, whether the asset in question is financial or the identity through which you access the financial system in the first place. That durability of choice is what creates optionality.

III. Optionality: Expanding the Range of Possible Choices

If resilience is about surviving uncertainty, and sovereignty is about preserving decision-making power, then optionality is about what becomes possible once both are established.

This is perhaps the least discussed dimension of Bitcoin’s value proposition — and potentially the most consequential for the audience that matters most to its next phase of adoption: asset managers, family offices, private banks, wealth advisors, and legal professionals working at the intersection of cross-border finance and long-term wealth preservation.

Sovereignty answers the question: Who decides?

Optionality answers the question that follows: What becomes possible once decision-making power is preserved?

Architecture, explored in the next section, answers a third: How do we scale those possibilities?

The progression matters because optionality is not merely a philosophical concept; it is the bridge between individual sovereignty and institutional capital markets. The standard Bitcoin narrative frames the asset primarily as a store of value or a hedge against monetary debasement. BTC Prague 2026 proposed a more precise and, for institutional purposes, more useful framing:

Bitcoin enhances the range of meaningful options for both individuals and institutions, going beyond just financial profits. It broadens the scope of decisions and the capabilities that Bitcoin enables across multiple dimensions simultaneously.

For High-Net-Worth Individuals and Family Offices

The ability to hold a globally liquid, seizure-resistant asset outside the banking system without sacrificing institutional-grade custody.

The ability to structure intergenerational wealth transfers that are not dependent on the legal framework of any single jurisdiction.

The ability to maintain liquidity and mobility in environments where traditional financial infrastructure is restricted, unstable or politically constrained.

For Entrepreneurs and Corporate Treasurers

The ability to access Bitcoin-backed credit structures, treasury strategies and emerging yield instruments as the regulatory framework matures.

For Financial Institutions

The ability to offer clients regulated exposure to Bitcoin through familiar investment vehicles — ETFs, structured products and tokenized funds — without requiring direct interaction with the underlying protocol.

These are not competing visions of Bitcoin. They are different expressions of the same underlying principle: the freedom to engage with Bitcoin through the model best suited to one’s objectives, constraints and time horizon.

BTC Prague repeatedly demonstrated that Bitcoin no longer implies a single participation model. Self-custody, institutional custody, treasury strategies, ETFs, Bitcoin-backed credit and tokenized financial products increasingly coexist as complementary expressions of the same underlying principle.

One conversation during BTC Prague 2026 illustrated this dynamic with particular clarity.

During a discussion with a legal practitioner working in Liechtenstein, one of Europe’s most sophisticated jurisdictions for digital asset structuring, a simple observation emerged:

At a certain level of complexity, wealth preservation eventually becomes a question of optionality.

The point was not ideological. It was strategic.

Jurisdictional diversification, succession planning, multi-currency liquidity, cross-border custody arrangements — these are not responses to a specific threat. They are responses to uncertainty itself. And Bitcoin is increasingly becoming a tool for managing that uncertainty across multiple planning horizons simultaneously.

Bitcoin is not merely an asset class. It is an option generator.

In this context, Bitcoin is more than just an asset class; it functions as an option generator. It broadens the scope of available structures, including cross-border trusts, digital asset inheritance plans, Bitcoin-backed credit facilities, multi-jurisdictional custody solutions, and regulated investment vehicles. For legal and compliance professionals, this perspective radically changes the discussion. The focus is no longer solely on whether their client should hold Bitcoin.

As Jack Mallers, founder and CEO of Strike, concluded in one of the conference’s closing keynotes:

“You know what we get to do when we leave here? We get to build things.”

Jack Mallers speaks at BTC Prague 2026

That challenge leads directly to the final theme emerging from BTC Prague 2026: architecture.

IV. Architecture: Transforming Bitcoin’s Possibilities into Scalable Financial Realities

If optionality expands the range of possible choices, and architecture transforms those choices into scalable financial realities, then this distinction is the defining challenge of Bitcoin’s current phase of development.

Resilience, sovereignty, and optionality describe what Bitcoin makes possible. Architecture describes how those possibilities become accessible — at institutional scale, across regulatory jurisdictions, through familiar financial instruments and within the legal frameworks that govern global capital allocation.

And what BTC Prague 2026 made visible, perhaps more clearly than any previous edition of the conference, is that this architecture is no longer being designed.

The industrialization of Bitcoin.

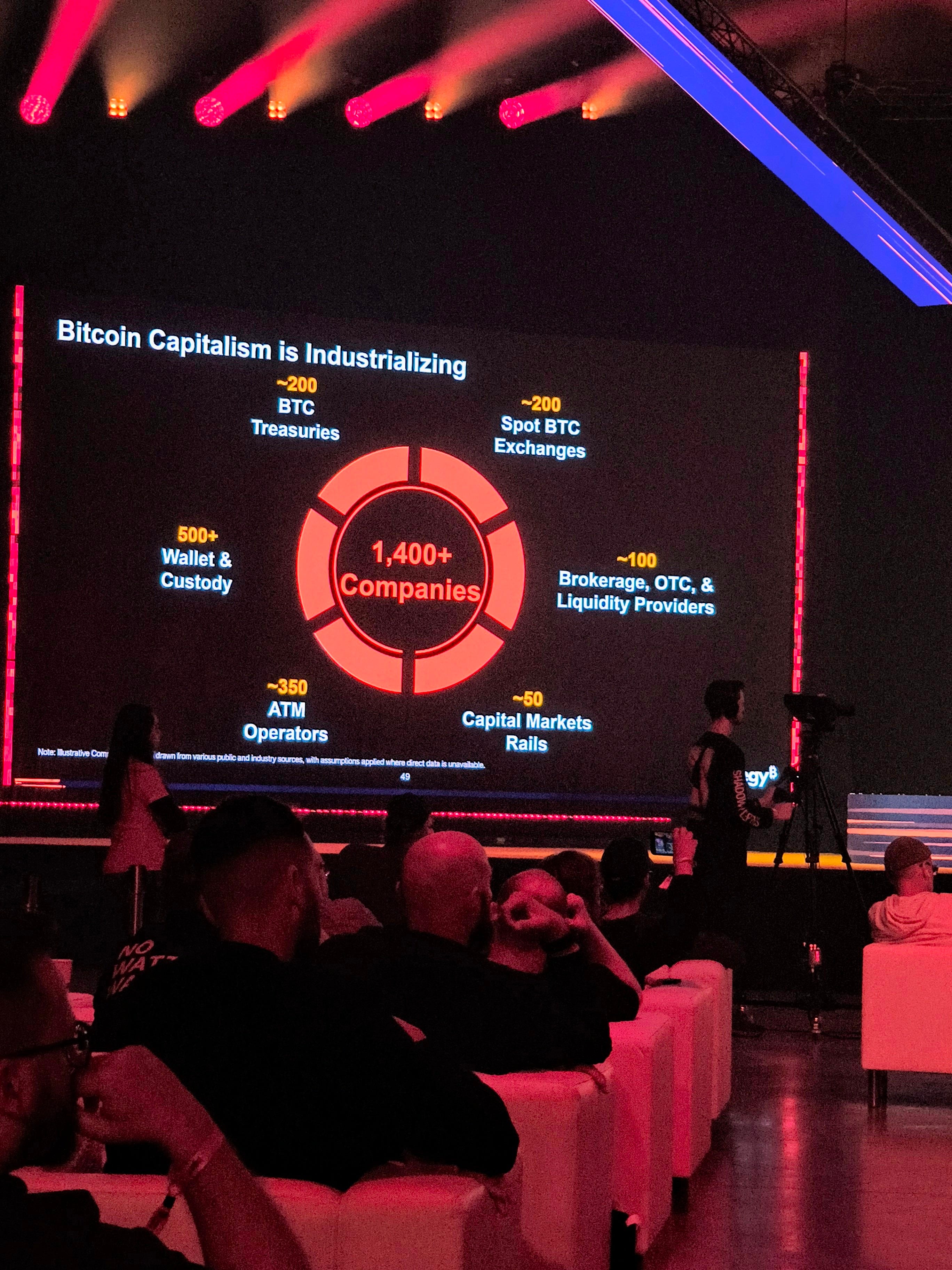

Michael Saylor’s keynote, Digital Capital, Equity, and Credit, provided the most systematic framework for understanding this industrialization.

His central thesis was deceptively simple:

The world does not lack capital. What it lacks are financial products capable of connecting that capital to Bitcoin.

Michael Saylor Speaks at BTC Prague

This reframing is significant for institutional readers. Most Bitcoin commentary assumes that the next wave of adoption will come from individuals buying Bitcoin directly. Saylor’s argument points elsewhere entirely.

The people sitting in conferences like Bitcoin Prague have already crossed the bridge. They understand private keys, custody, volatility, and long-term conviction. The next trillion dollars will not come from them. It will come from pension funds, insurance companies, sovereign wealth funds, corporate treasuries, family offices, wealth managers, and banks.

Institutions are not looking for Bitcoin. They are looking for products.

One of the most revealing frameworks discussed throughout BTC Prague did not focus on Bitcoin itself, but on the architecture surrounding it: Asset, Function, Custody, Jurisdiction, Distribution, Form, Risk, Liquidity, Investor Characteristics.

Each dimension represents a layer of decision-making that determines how a specific category of investor can legally, operationally, and financially access Bitcoin.

The framework highlighted a critical reality: Bitcoin adoption will not be determined solely by the properties of the underlying asset. It will be shaped by the legal, financial, and operational forms through which different categories of investors access it.

A retail investor may access Bitcoin through a self-custody wallet.

A high-net-worth individual may access it through a separately managed account or a trust structure.

A pension fund will access it through a regulated fund vehicle that meets specific custody, insurance, and governance requirements.

A corporate treasury will hold it as a balance sheet asset subject to accounting standards and board governance frameworks.

An entrepreneur will build financial products on top of it.

Same asset. Fundamentally different architectures of interaction.

Saylor described an emerging financial stack organized as a hierarchy of interdependent layers:

Digital Capital (Bitcoin): the foundational collateral layer, finite, portable and globally liquid.

Digital Credit: lending, borrowing and credit structures collateralized by Bitcoin.

Digital Money: liquidity and monetary instruments built around Bitcoin capital markets.

Digital Yield: income-generating products built on top of the underlying layers.

Bitcoin becomes not simply an asset to be held, but the collateral layer of an entirely new financial architecture.

In Saylor’s framework, Bitcoin is increasingly positioned not as digital currency, but as digital capital — a foundational asset capable of supporting multiple layers of credit, liquidity and financial products.

(Source: Michael Saylor, BTC Prague 2026 keynote)

One slide from the presentation captured the scale of what is already underway: more than 1,400 companies now operate across the Bitcoin ecosystem — approximately 200 corporate Bitcoin treasuries, 200 spot exchanges, 500 wallet and custody providers, 100 brokerage and liquidity providers, 350 ATM operators and around 50 capital markets infrastructure companies.

Slide from Michael Saylor’s Keynote at BTC Prague 2026

Bitcoin capitalism, as Saylor framed it, is industrializing.

This is not simply growth. It is the emergence of a structured industry — with specialized roles, regulated intermediaries, compliance frameworks and institutional-grade infrastructure — built on Bitcoin as its foundational asset.

But Saylor’s presentation also contained a more demanding insight, one that several other sessions at Prague reinforced independently. Bitcoin alone is not sufficient to attract global capital. Global capital requires compliance, custody, insurance, governance, legal certainty and familiar investment vehicles.

This is not a critique of Bitcoin, this is simply a description of how capital markets actually function. A pension fund cannot allocate to an asset without a regulated custody solution, an auditable legal structure and a clear regulatory classification.

A family office cannot hold Bitcoin across generations without robust inheritance frameworks and multi-jurisdictional legal certainty. A corporate treasury cannot carry Bitcoin on its balance sheet without established accounting standards and board-level governance frameworks. These requirements are not obstacles to Bitcoin adoption. They are the architecture of adoption.

Several sessions at BTC Prague 2026 addressed the practical dimensions of this infrastructure build-out directly

On custody: key control, withdrawal rights, asset segregation, rehypothecation risk, counterparty exposure, regulatory status and operational resilience were identified as interdependent components of a coherent institutional custody framework — not separate issues to be addressed individually.

On capital markets: the emergence of Bitcoin treasury companies — corporations holding Bitcoin as their primary balance sheet asset — was presented as a new asset class combining Bitcoin exposure with equity market liquidity. The model is being replicated across multiple jurisdictions. (See Bitcoin Treasuries for a current overview of publicly listed Bitcoin treasury companies :

On tokenization and real-world assets: Bitcoin-backed credit structures, tokenized investment vehicles and regulated digital asset funds are no longer theoretical constructs. They are operational products in an increasing number of jurisdictions. The same architectural logic underpinning Bitcoin’s institutional infrastructure, including custody, legal certainty, distribution frameworks, investor protections and scalable market infrastructure, is equally foundational to the tokenization of real-world assets and digital securities. More broadly, for participants in the RWA ecosystem, Bitcoin’s industrialization is the same infrastructure build-out, applied to the most liquid and globally recognized digital asset in existence.

On regulation: MiCA, DAC8 and equivalent frameworks were referenced repeatedly, not as constraints but as enabling conditions. Legal certainty, for institutional allocators, is a prerequisite for meaningful capital deployment. Europe’s regulatory framework is increasingly seen as providing what global capital requires before it moves: a clear, stable set of rules within which to operate (See Regulation (EU) 2023/1114 (MiCA) and Directive (EU) 2023/2226 (DAC8): https://eur-lex.europa.eu/eli/reg/2023/1114/oj, and https://eur-lex.europa.eu/eli/dir/2023/2226/oj

A conversation at BTC Prague 2026 with a senior executive from a large digital asset infrastructure provider highlighted an often-overlooked dimension of institutional demand: provenance.

As institutional participation expands, the question is no longer only whether Bitcoin is authentic, but how institutions document, verify and report the pathway through which it was acquired. At the protocol level, one bitcoin is equivalent to any other bitcoin, yet for certain institutional participants, the acquisition pathway matters. Regulatory scrutiny, audit requirements, internal compliance procedures and risk management frameworks are creating demand for Bitcoin sourced through transparent and verifiable channels.

In this context, mining infrastructure is evolving beyond simple asset production. It is becoming part of a broader trust architecture capable of providing institutions with direct access to newly mined Bitcoin and simplified provenance verification.

This creates a different form of access, not a different form of Bitcoin

The implication is significant: trust in institutional Bitcoin markets is created by regulation and provenance, and increasingly both are required. Regulatory frameworks define the rules. Provenance documentation provides the evidence. Both are becoming part of the architecture of institutional adoption.

As Bitcoin capital markets mature, institutions are increasingly selecting not only an asset allocation strategy, but an access architecture: self-custody, regulated custody, ETFs, treasury companies, Bitcoin-backed credit facilities, tokenized investment vehicles, or direct acquisition through verifiable production channels. The result is not the emergence of multiple Bitcoins, but the emergence of multiple architectures surrounding a single monetary asset. The architecture being built around Bitcoin today is the institutional expression of its foundational principles.

Bitcoin proved that resistance is possible. Now we build the rest.

The architecture being built today — custody, compliance, capital markets rails, tokenized vehicles and regulated distribution — is precisely that: the rest.

Self-custody and regulated custody serve different needs within the same ecosystem.

Sovereignty and compliance operate at different scales within the same legal reality.

Individual optionality and institutional infrastructure are complementary layers of the same emerging financial architecture.

The next phase of Bitcoin adoption will therefore be determined less by the asset itself than by the quality of the architectures built around it.

And that architecture, regulatory, financial, operational and legal, is what will ultimately determine the speed, scale and shape of Bitcoin’s integration into global capital markets.

The question was never whether Bitcoin would be adopted. It was whether the infrastructure around it would be built to scale. That infrastructure is now being built.

Every major Bitcoin conference leaves behind a dominant narrative.

BTC Prague 2026 left behind something different.

Not a single narrative. A structural insight.

The four themes that ran through the conference, resilience, sovereignty, optionality and architecture, are not parallel observations. They are a sequence - a form of logic that points towards something more fundamental. Resilience makes sovereignty possible. Sovereignty makes optionality real. Optionality makes architecture necessary.

Resilience preserves systems against uncertainty.

Sovereignty preserves the power to make meaningful decisions.

Optionality expands the range of decisions available.

Architecture transforms those possibilities into scalable economic realities.

The question that emerges from this chain is not which model of Bitcoin adoption will prevail but what kind of ecosystem emerges when all four coexist.

Multiple Architectures, One Asset.

BTC Prague 2026 suggested that Bitcoin is becoming large enough to support several architectures simultaneously, evolving beyond a single model.

The debate is no longer simply between Bitcoin and the traditional financial system.

It is increasingly about the different ways individuals and institutions choose to interact with Bitcoin, and the infrastructure being built to make each of those participation models viable at scale.

Some will choose self-custody, long-term savings and intergenerational wealth transmission outside the traditional financial system.

Some will choose regulated custody, ETFs and familiar investment vehicles that provide Bitcoin exposure without direct interaction with the underlying protocol.

Some will hold Bitcoin as a primary treasury asset on a corporate balance sheet.

Others will access it through Bitcoin-backed credit structures, digital yield products or tokenized financial instruments.

Others still will build the custody solutions, compliance frameworks and capital markets infrastructure that makes all of the above possible for everyone else.

These paths are often portrayed as competing visions.

BTC Prague 2026 suggested they may instead be complementary expressions of the same underlying principle: the preservation of freedom through choice.

An individual may choose to hold Bitcoin in self-custody for long-term savings, inheritance and wealth preservation. The same individual may also choose to access Bitcoin-powered financial products for entrepreneurship, investment, liquidity or corporate finance.

These decisions reflect different objectives, constraints and time horizons, different architectures of participation in the same ecosystem.

The maximalist and the institutional allocator are not adversaries.

The self-custody advocate and the ETF investor are not contradictions.

The sovereign individual and the regulated treasury manager are not opposites.

They are, increasingly, participants in the same ecosystem, — interacting with the same underlying asset through frameworks suited to their own values, constraints and long-term objectives.

Beyond markets, products and infrastructure, a recurring theme throughout BTC Prague 2026 was the importance of designing systems with multi-decade time horizons in mind.

Whether discussing post-quantum resilience, intergenerational wealth transmission, digital identity infrastructure or long-term treasury strategies, the conference repeatedly returned to the same underlying challenge: building systems that can endure technological, regulatory and geopolitical change over time.

In that sense, Bitcoin may be evolving from a simple asset into an option generator.

Not because it eliminates constraints, but because it expands the range of meaningful choices available to individuals and institutions alike.

This may be the clearest lesson BTC Prague 2026 leaves behind.

Bitcoin’s next phase will be defined by the coexistence of multiple architectures of participation.

And the freedom to choose among them may ultimately prove to be one of Bitcoin’s most important — and most enduring — forms of value.

Because in the end, sovereignty is the freedom to choose how to participate in the future being built around it.

Thanks for reading! Subscribe for free to receive new posts and support my work.

About the author

Ruben Landsberger is a French lecturer, consultant and former international tax lawyer with a focus on digital assets, tokenization, blockchain regulation and emerging financial infrastructures. He attended Consensus Miami and BTC Prague 2026 and recently moderated a panel on blockchain, finance and post-quantum security at the Q-Day Summit in Paris. He holds a DeFi Expert certification from Alyra (RS6675).