America's Legislative Architecture Wasn't Built for This

What TEFRA, Basel III, and stablecoin settlement mean for tokenization - and why the current legislative stack falls short

Last week's piece on the March 25th House Financial Services Committee hearing generated a response worth addressing directly. In the days following the post, some of the commentary noted how important the TEFRA angle was, and one commenter said this was “proof that legacy legislation still has a long way to catch up.” They weren’t wrong, which is why we’re diving into this follow-up.

Here's the short version of what this piece is about. The US is building financial infrastructure for tokenized assets at a pace that outpaces the legal and regulatory frameworks meant to govern it. The legislation everyone is watching - the CLARITY Act - addresses some of that gap. It leaves the most structurally consequential constraints entirely untouched. What follows is a map of those constraints, their costs across different types of participants, and what catching up actually requires beyond the bill dominating the conversation. If you work in private equity, venture capital, wealth management, or institutional finance and are trying to understand what the regulatory picture actually means for decisions being made right now, this piece is written with you in mind.

That observation brings into focus something this hearing, and likely future hearings, won’t be able to address on their own. The challenge facing tokenization isn’t rooted exclusively in the fact that Congress is slow, regulators are hostile, or institutional capital is reluctant.

From the beginning, financial oversight in the United States was architected for a world where innovation happened inside the regulated intermediaries that govern monetary movement, assets, and debts, specifically banks, broker-dealers, and exchanges, entities that could be supervised, examined, and held accountable through existing frameworks. I've explored both the trust dynamics and the infrastructure constraints behind this in depth across two earlier pieces: “Are We Undervaluing RWAs by Thinking Too Narrowly?” and “Tokenization, Legacy Cores, and the Next Financial Revolution.”

The monolithic cores that have long protected their own architecture have done so at the expense of the structural change needed to move toward atomic settlement, and with it, the broader possibilities that architecture makes accessible. These include tokenized issuance-based product strategies such as real-time portfolio, distributed fractional ownership, and other mechanisms that open asset classes to participants the current system structurally excludes, as well as share-of-wallet dynamics that shift when settlement is no longer a barrier to participation.

That moment is now upon us. Protocol layers beyond those intermediaries are doing meaningful work, but until oversight can keep pace with the revisions the market requires, guidance, exemptive relief, and iterative rulemaking will only ever address symptoms. That brings into focus the underlying mismatch between a framework built for intermediaries and a market that has moved beyond them.

That distinction has direct consequences for everyone making decisions right now. Founders calibrating timelines and deployments, institutions evaluating counterparties, and advisors explaining products to clients are all operating on the assumption that regulatory clarity is needed and forthcoming. The first part of that assumption is correct. The second depends entirely on which constraint you’re looking at, and for several of the most consequential ones, the current legislative architecture is not capable of delivering resolution on any near-term timeline.

So What Did the Hearing Actually Confirm?

The March 25th, 2026, session put two things on the record that matter, and it’s worth being specific about what they were and weren’t.

Chairman French Hill described tokenization as a structural transformation in how securities are issued, traded, and recorded, the first time a committee chair has placed that characterization formally into the congressional record. The acknowledgment was bipartisan, which means the political cover for inaction is shrinking. Six months ago, neither of those things was true. For anyone watching this space, that’s meaningful progress.

What the hearing didn’t do was address the constraints that actually determine how fast this market grows and who gets to participate. Most of those constraints don’t live in the same legislative lane as the CLARITY Act. Understanding which ones the bill touches and which ones it doesn’t is more useful right now than tracking its Senate floor prospects.

TEFRA - The Elephant in the Room

The largest asset class in the world is bonds. Tokenizing them at scale in the US has a specific legal problem that predates crypto by four decades, sits in tax law rather than securities law, and isn’t addressed by any bill currently moving through Congress. That problem is TEFRA, the Tax Equity and Fiscal Responsibility Act of 1982, and it’s the constraint that received almost no public attention after the hearing despite being named directly in testimony.

Congress wrote TEFRA to prevent bearer bond abuse. Forty-four years later, it inadvertently prohibits tokenized bond issuance on permissionless public blockchains, because peer-to-peer wallet transfers are functionally indistinguishable from bearer instruments under its current language. Whatever the policy intent, the enforcement outcome is concrete: denial of interest deductions, excise taxes at issuance, reclassification of capital gains as ordinary income, and 30% withholding on interest payments regardless of where the investor is based.”

If your fixed-income tokenization architecture routes transfers between self-custodied wallets on a permissionless public chain, has your tax counsel specifically analyzed that transfer mechanism against TEFRA's definition of a bearer instrument, not just your securities counsel against registration requirements? Those are different reviews addressing different statutory frameworks, and a clean securities-law analysis does not clear your TEFRA exposure. When your cap table or institutional partners ask about regulatory risk, is TEFRA in that conversation? If it isn't, the more important question is whether it's absent because it was analyzed and resolved, or because nobody on either side of the table knew to look for it.

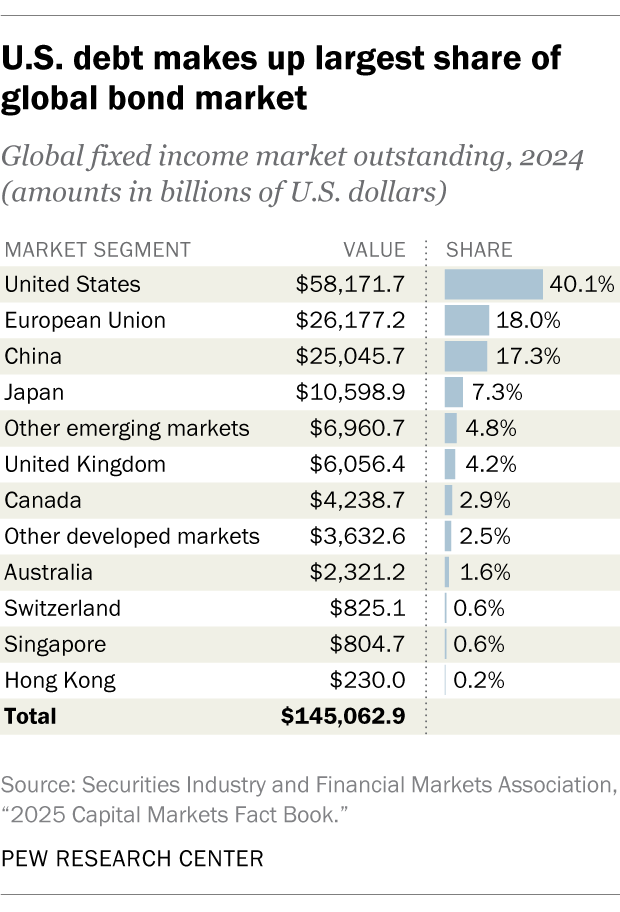

The global bond market represents $145.1 trillion in outstanding fixed-income securities, per the Securities Industry and Financial Markets Association's 2025 Capital Markets Fact Book, a figure cited directly in Salman Banaei's testimony before the Committee on March 25. The United States holds the largest share at $58.2 trillion, or 40.1% of the global total. The European Union holds $26.2 trillion at 18%, the United Kingdom $6.1 trillion at 4.2%, and Singapore $804.7 billion at 0.6%. Those are not small peripheral markets. The EU alone holds nearly half the US share of global bond debt. All three are actively building regulatory frameworks to capture tokenized bond issuance. The reason the US isn't leading that development despite holding the world's largest bond market isn't technology or institutional appetite. It's a 1982 tax statute that nobody in the current legislative conversation has a vehicle to fix.

It's worth addressing a recent development that might appear to complicate this picture. The New Hampshire Business Finance Authority's bitcoin-backed bond, which received a provisional Ba2 rating from Moody's, doesn't change the TEFRA analysis. That structure routes through a traditional state conduit issuer with bitcoin held in custody by BitGo as collateral. It is a traditional bond backed by crypto, not a tokenized bond issued on a permissionless public blockchain with peer-to-peer wallet transfers between self-custodied wallets. TEFRA's bearer instrument problem is triggered by the latter, not the former. What the New Hampshire deal actually illustrates is the workaround: you can bring crypto into the bond market by routing it through traditional infrastructure. That is precisely the needle-threading dynamic this piece describes elsewhere, and it underscores rather than resolves the structural gap TEFRA creates for permissionless chain issuance.

When you evaluate a tokenized fixed-income product, does your due diligence process include a review of the issuance structure against TEFRA, or does it stop at custody standards, securities classification, and AML compliance? A clean custody and securities analysis doesn't tell you whether the issuer has a TEFRA problem. It tells you about a different set of risks entirely.

Banaei named it directly in his testimony. It got almost no coverage afterward, partly because it doesn’t fit the CLARITY Act narrative that dominates this space, and partly because it falls under tax law rather than securities law, putting it entirely outside the committee’s jurisdiction. Worth noting that Banaei testified as General Counsel of Plume Network, the same infrastructure layer behind the payroll pilot described earlier in this piece, which means the firm making the case for TEFRA reform at the congressional level is also the one demonstrating what compliant tokenization looks like in practice when TEFRA isn’t the blocking constraint. A statutory barrier material enough to affect the competitiveness of US fixed-income markets sits in a different legislative lane than the bill everyone is watching, and nobody is coordinating the two lanes. That’s a capacity failure, and it’s exactly what observations following the congressional hearing have pointed to.

The practical question for anyone in this space isn’t whether TEFRA gets fixed. It’s whether your current architecture assumes it already has been, and what that assumption is currently costing you in both directions.

The defensive cost is proximate. For founders, TEFRA exposure is most likely to surface during institutional due diligence or a fundraising process, at the moment when an architecture rebuild is most disruptive and most visible to the counterparties whose confidence you’ve spent months building. For institutions, the denial of the portfolio interest exemption triggers 30% withholding on interest payments regardless of investor residence, and if your fund has non-US limited partners receiving yield from a TEFRA-exposed tokenized bond product, that obligation doesn’t stay with the issuer. For advisors, the cost is the client conversation that follows a restructuring or an unexpected tax consequence, where the honest answer to “why didn’t you flag this?” is that the statutory risk was never part of your review process. That conversation is recoverable once.

The opportunity cost runs in the other direction. A founder who can demonstrate a TEFRA-clean structure specifically and technically to a major fixed-income asset manager is in a different conversation than one who can’t, and that’s a distribution conversation, not a compliance one. Institutions that develop a TEFRA-specific evaluation framework now are the ones that can move quickly when TEFRA-clean fixed-income tokenization reaches allocatable scale. For advisors, understanding TEFRA’s implications isn’t a defensive capability. It’s the basis for a substantively different conversation with clients, one where you can explain which structures are clean, which aren’t, and why that distinction matters, before the client finds an advisor who can.

Singapore, the UK, and the EU are not waiting for the US to coordinate its legislative lanes. The firms that understand the specific constraints operating in that window are the ones that will still be in the room when it closes.

The CLARITY Act Situation Has Gotten More Complicated

Since last week’s piece was published, there are four things worth bringing to the surface.

1. The stablecoin yield text survived recess unrevised

The Senate went into Easter recess on March 30th, 2026, with the stablecoin yield text unrevised, despite expectations that a compromise draft would emerge before the break. As FinTech Weekly reported, the bill entered the April 13 return carrying bank-friendly yield language that Coinbase and Stripe have both formally objected to. The text bans passive yield on stablecoin balances, permits only narrowly defined activity-based rewards, and gives the SEC, CFTC, and Treasury twelve months to define what counts as permissible.

Since then, the picture has shifted. On April 1st, 2026, Coinbase’s chief legal officer, Paul Grewal, described negotiations as “very close to a deal” - the most significant public signal of movement since January. Behind the scenes, senators are expected to release revised final text this week, per Crypto In America, detailing how crypto firms can offer activity-based rewards without triggering deposit flight from banks. Whether that text resolves Coinbase’s core objection or simply narrows the gap remains to be seen. As Elliptic noted, the compromise has met mixed reviews from the crypto industry, and stablecoin yield is not the only outstanding issue - Senate Democrats are still pushing for ethics language barring government officials and their families from crypto-related conflicts of interest.

2. The White House no longer has a crypto czar, but Sacks hasn't left entirely

{kind=link}

David Sacks confirmed on March 26 that his 130-day term as White House AI and crypto czar has expired. He is not disappearing from the administration entirely - he is moving to co-chair PCAST alongside Michael Kratsios, retaining a direct line to the President on technology policy. Patrick Witt, who served as Executive Director of the White House Crypto Council under Sacks, also remains in position.

But the distinction between the two roles matters. PCAST produces reports and recommendations. It does not negotiate legislative text with Senate staff or broker compromises between banking lobbyists and crypto executives in closed-door Capitol Hill sessions. The most consequential stretch of digital asset legislation in years now moves without a dedicated White House operational advocate driving it from inside the administration -and as Unchained reported, Sacks’ departure closes a tenure that reshaped the federal government’s posture toward digital assets but left its biggest deliverables unfinished.

3. The advisory infrastructure that remains tells its own story

As FinTech Weekly reported, Marc Andreessen and Fred Ehrsam - both of whom publicly backed the CLARITY Act in January despite the stablecoin yield restrictions, at the moment when Coinbase's withdrawal threatened to collapse the bill - are PCAST members.

Ehrsam co-founded Coinbase but left in 2017 and now runs Paradigm, one of the largest crypto-native venture capital firms. His position on the bill reflects portfolio-wide benefits from regulatory clarity rather than Coinbase's specific revenue exposure to the yield restriction. Brian Armstrong is not on PCAST. The President's senior technology advisory structure is now populated by the faction that accepted the bank-friendly yield compromise as the price of a broader legislative framework, and as FinTech Weekly noted, a Coinbase whose second objection has cost it significant political capital it spent years building inside Washington, enters the April markup window in a weaker negotiating position than it held in January. When April's markup negotiations resume, the starting position is not neutral. It is the draft that survived recess unrevised.

4. The timeline is compressing, and the bill is picking up political baggage

Senator Lummis has confirmed the markup is targeted for the second half of April, with the weeks of April 13th and April 20th as the only remaining windows before Senator Moreno’s deadline. His warning is still on the record: miss the Senate floor by May, and digital asset legislation may not move again for years. The community bank deregulation attachment adds another layer of complexity. As FinTech Weekly reported, Senate Banking Republicans are discussing attaching community bank deregulatory provisions to the bill in exchange for the House accepting the Senate’s housing package, pulling it into a negotiation that has nothing to do with tokenization. American Banker confirmed on April 1st that House Financial Services Chairman French Hill has personally flagged this dynamic, noting that two of his primary pieces of legislation on digital assets and housing remain blocked in the Senate - underscoring that the political trade is real and compressing an already narrow timeline.

The stablecoin yield impasse is worth reading as an illustration of the capacity problem rather than a separate political dispute. Stablecoins are simultaneously yield-bearing instruments and payment instruments, and the legislative architecture was built for a world where those were distinct categories. Both sides are making coherent arguments within their own frameworks. Whatever compromise eventually emerges will be a workaround negotiated within an inadequate framework, not a resolution of the underlying structural mismatch. The impasse persists in its current form precisely because the framework lacks a mechanism to resolve it cleanly.

What Compliance by Needle-Threading Actually Tells Us

This week produced a concrete example of what working within these constraints looks like for a well-resourced team. Plume, Toku, and WisdomTree announced the first payroll pilot using a tokenized money market fund, WTGXX, as a compensation delivery mechanism. Employees can elect to receive a portion of their salary in tokenized fund shares that begin earning yield from the day of payment, without touching crypto exchanges or purchasing digital assets directly.

It works. And it works because every layer routes through an existing regulated wrapper: WisdomTree Digital Trust Company, chartered as a limited purpose trust company by the New York State Department of Financial Services; its federally registered money services business and NMLS registration; its prospectus disclosures for WTGXX; its AML-verified WisdomTree Prime wallet infrastructure; and its established eligibility requirements for account holders. As Toku CEO Ken O’Friel put it:

“Every payroll provider in the last 30 years has improved the UI and UX, but they’re all built on the same legacy financial infrastructure that hasn’t changed since the 1970s.”

The pilot shows that tokenization can add real utility within existing frameworks, specifically yield from the moment compensation is paid, without disrupting how payroll runs. It also shows that doing this compliantly requires assembling a multi-entity regulated infrastructure stack that only well-resourced firms with established institutional relationships can build. The broader market that the hearing was nominally about doesn’t have access to that stack. A framework that operates through needle-threading by sophisticated actors is not designed to govern the market at scale.

What This Means for the Decisions Being Made Now

For founders and builders

The constraints requiring separate Congressional action, specifically TEFRA, Basel capital surcharges applying a 1,250% risk weight to permissionless blockchain assets, and stablecoin settlement infrastructure, will not be resolved by CLARITY Act passage, even in the most optimistic scenario.

Has your architecture been stress-tested against Basel’s 1,250% risk-weight treatment for permissionless blockchain assets specifically? That constraint affects whether the banks and institutional counterparties you’re building toward can participate in your market at all without a capital hit that makes participation commercially unviable. If they can’t hold your asset without a punitive capital charge, your distribution strategy has a structural ceiling that no amount of product quality resolves.

On stablecoin settlement: if your tokenized product requires a cash leg for on-chain settlement, which stablecoin serves that function, under what regulatory classification, and what happens to your settlement architecture if pending legislation reclassifies the instrument you’re currently using? Have you modeled that scenario, or is your settlement assumption built on the current state of a market that is actively being legislated?

On operational readiness: if your product implies real-time settlement, does your compliance, reporting, and risk infrastructure actually operate at that speed? Settlement compression changes when compliance obligations, margin calls, and counterparty exposure calculations are completed, not just when assets move. If your back-office infrastructure was built for T+1 or T+2 cycles, the gap between that and what your product promises creates operational risk within your architecture, regardless of how clean your legal structure is.

The founders who will define institutional-grade tokenization infrastructure are the ones who can answer those questions specifically. The bill matters. It doesn’t resolve your constraint stack.

For institutions

Sandy Kaul’s taxonomy covering synthetic exposure tokens, digitally native structures, and digital twin models remains a more operationally useful due diligence lens than tracking the CLARITY Act’s Senate prospects, because it maps directly to where ownership rights, settlement finality, and counterparty exposure actually land in each structure. For the full original analysis, see Kaul’s Detangling Tokenization of RWAs, published March 24th, 2026. Worth noting that Kaul’s is one of several classification frameworks now in use.

The joint SEC-CFTC interpretive release published March 17th, 2026, uses a five-category taxonomy that includes digital commodities, digital collectibles, digital tools, stablecoins, and digital securities, which are organized around regulatory jurisdiction rather than ownership structure. For the purpose of this article and the proceeding applications, we use Kaul’s here because ownership rights and settlement mechanics are where the due diligence questions that matter most to institutional allocators actually live.

The model determines the failure mode, the custody obligation, and the recourse available if the structure fails. Knowing which model you’re in is the starting point, not the conclusion.

For synthetic exposure tokens: what is the SPV structure underlying this token, who controls it, under what jurisdiction is it governed, and what is the redemption mechanism if the issuing entity faces liquidity stress? On-chain settlement finality doesn’t eliminate the off-chain settlement timeline of the underlying asset. If the underlying asset settles T+1 or T+2 and your on-chain representation shows immediate finality, that gap is counterparty exposure you are carrying, whether or not your reporting reflects it.

For digital twin structures: what batch settlement cycle governs the authoritative off-chain record, and what happens to your position during the window between a token transfer on-chain and the corresponding update in the off-chain ledger? That window is an interval of ownership ambiguity, and under stress, ownership ambiguity in fixed-income markets has historically been where losses have concentrated.

For digitally native structures: if the token is permissioned, what happens to your position if a wallet verification lapses, a counterparty fails a KYC refresh, or the permissioning infrastructure experiences an outage? The composability you gave up for regulatory alignment comes at a cost that only becomes visible under pressure.

Two infrastructure questions apply across all three models. First, counterparty concentration: if the product relies on a single oracle network for its reference price, what happens to NAV calculation, margin calls, and redemption mechanics if that oracle experiences an outage or manipulation? Infrastructure concentration risk doesn’t surface in standard securities due diligence, and doesn’t disappear because the product has a clean legal structure.

Second, cross-jurisdictional enforceability: under which legal framework is ownership determined in a dispute when the product involves issuers, custodians, or counterparties across multiple jurisdictions? UCC Article 12 governs digital asset ownership in adopting states, but adoption is uneven, and its interaction with non-US frameworks remains largely untested. Has your legal team mapped that for each product you hold?

For advisors and wealth managers

The most immediate gap is between what clients believe they own in a tokenized product and what the underlying legal structure actually provides. This isn’t a new problem. MF Global filed for bankruptcy on October 31, 2011, the eighth largest in US history, with a $1.6 billion shortfall in customer funds legally required to be held in segregated accounts. As a Congressional investigation found, customers correctly understood the risks of their trading activity. What they didn’t anticipate was that the segregated accounts protecting them were themselves at risk. The legal requirement existed. The protection it was supposed to provide did not.

Tokenization doesn’t create that failure mode. Depending on the model, it inherits it or amplifies it, and in synthetic structures, the gap between on-chain presentation and legal reality can be harder to see coming than it was for MF Global’s customers.

If a client holds a synthetic exposure token and the issuing SPV faces redemption pressure, what is their actual position in the redemption queue, and is that documented in the product disclosure they received? If the redemption mechanics are under stress and aren’t clearly disclosed, that is a gap in your due diligence process, not the client’s understanding.

If a client holds a digital twin token and asks what they own, can you explain which record governs in a dispute, the on-chain token or the off-chain ownership record, and under what legal framework? If your answer relies on the on-chain representation, you are explaining a receipt rather than an ownership right.

If a client asks whether their tokenized product is covered by SIPC, FDIC, or any equivalent protection, do you know the answer for the specific model and custody structure? The answer varies by model, custodian, and jurisdiction, and “I’ll find out” is not a sustainable posture for a product category your clients are increasingly asking about.

For internationally mobile clients or those with cross-border estate planning considerations: how are their tokenized products treated under each relevant jurisdiction’s property and succession law? The gap between what an on-chain position shows and what a foreign court would recognize as an enforceable claim is largely untested. That’s an estate-planning risk sitting inside products presented as simple and accessible.

On reporting: can your infrastructure reflect your client’s tokenized positions accurately enough to explain their holdings, yield accrual, and exposure at any point on any given day? If your reporting runs on T+1 or end-of-day cycles and the product accrues yield continuously, there is a gap between what your reporting shows and what your client actually holds. That gap is manageable until a client asks a specific question at the moment the gap is widest, which is usually when markets are moving.

Advisors who build the capability to answer these questions specifically and in advance are building a durable practice in a market early enough that the capability is genuinely differentiating. The ones who don’t are carrying client relationship risk that surfaces at the worst possible moment: when the client needs the answer, and the market is under stress.

What Catching Up Actually Requires

Observations and commentary following the congressional hearing frame this as a gap between where legislation is and where it needs to be. The bills currently in motion, the CLARITY Act, the two draft bills from the March 25 hearing, and the PARITY Act, address jurisdiction, market structure, and recordkeeping. They are necessary. They are not sufficient.

Worth noting that the PARITY Act has moved meaningfully since the hearing. On March 26, Representatives Miller and Horsford released an updated discussion draft with significant revisions and stated their intention to formally introduce it as legislation this spring. The updated draft addresses stablecoin tax treatment, income deferral for staking and mining, wash-sale rules, and mark-to-market accounting for traders. That is genuinely useful progress on digital asset tax clarity. It does not touch TEFRA.

Modern legislation capable of governing this market would need to address three fronts not currently covered by any active legislative vehicle.

The First Gap - TEFRA

The first is TEFRA. As FinTech Weekly reported in its analysis of Larry Fink’s 2026 shareholder letter, no regulator can fix TEFRA by interpretation. It requires Congress to amend the relevant provisions of the Internal Revenue Code to recognize distributed ledgers meeting prescribed standards as valid bond registers. That task is not in the CLARITY Act. It is not in the PARITY Act, which addresses digital asset tax treatment in a different part of the tax code - stablecoin exemptions, staking deferral, and wash sale rules - and does not address the bearer-instrument provisions that make permissionless chain-bond issuance legally precarious. It is not in either of the draft bills from the March 25th hearing.

But here are a few questions worth ruminating on even after that amendment passes:

What does cross-jurisdictional tax treatment look like for tokenized bonds held by foreign investors under a reformed framework - specifically, does IRC amendment on distributed ledger recognition interact cleanly with the portfolio interest exemption that currently triggers 30% withholding?

How do state UCC Article 12 adoptions interact with a federal IRC amendment when the two frameworks were written without reference to each other? Debatably a question that has become more concrete since New York signed Article 12 into law on December 5, 2025, effective June 3rd, 2026 - the largest financial jurisdiction in the US now operates under a state digital asset ownership framework that has no federal IRC counterpart addressing the same instruments.

When does the tax event on a token transfer actually occur under reformed IRS guidance - at on-chain confirmation, at the off-chain record update, or at some other point in a settlement cycle that no longer maps cleanly onto either? The PARITY Act's updated draft, released March 26th, addresses stablecoin exemptions and staking deferral. It does not address settlement timing for tokenized bond transfers.

TEFRA reform opens the second layer of questions the market isn’t asking yet, the second is Basel.

The Second Gap: Basel

The second is Basel. The Basel Committee’s 1,250% risk weight on permissionless blockchain assets has moved from a future constraint to an active regulatory proposal. On March 19, 2026, the Federal Reserve, OCC, and FDIC formally proposed implementing the final phase of Basel III, retaining the 1,250% risk weight for permissionless blockchain assets, with a public comment period running through June 18, 2026. The Bank of England has delayed its own implementation to January 2027 to watch how US rulemaking develops, while Hong Kong and Canada implemented the standard on January 1, 2026, and the EU has partially implemented it. The Basel Committee itself has endorsed a targeted review of the cryptoasset standards, but that process is international and slow.

The practical constraint for anyone building tokenized fixed-income infrastructure on permissionless chains is that the 90-day comment period is the only near-term window to influence the US final rule's treatment of these assets. If the final rule retains the 1,250% weight without carving out tokenized traditional assets from pure crypto exposures, bank participation in permissionless chain tokenization remains commercially unviable regardless of what the CLARITY Act resolves. And if the US final rule diverges from Hong Kong’s already-implemented standard, cross-border tokenized fixed-income positions face differing capital treatment depending on which side of the transaction the bank sits on. Regulatory arbitrage in that environment is a structuring incentive, and structuring incentives in fixed-income markets have a documented history of producing concentrations of risk in places the framework wasn’t designed to see.

The Third Gap: Stablecoin Settlement Infrastructure

The GENIUS Act addressed stablecoin issuance and reserve requirements. Its implementation is now underway: the OCC’s proposed rule establishing a comprehensive supervisory framework for payment stablecoins has a comment deadline of May 1, 2026, and the Treasury formally initiated the GENIUS Act rollout on April 1, opening a 30-day registration window for existing issuers. The GENIUS Act also formally specifies that non-compliant stablecoins cannot serve as settlement assets for wholesale payments between banking organizations. What the GENIUS Act does not address is the structural question of what happens to atomic settlement when the cash leg itself is under stress.

Traditional T+1 and T+2 settlement cycles create float - a buffer between trade execution and final settlement that the entire architecture of traditional finance depends on. That window allows positions to be netted, collateral to be moved, margin calls to be met, and liquidity to be sourced before final obligations fall due. Clearinghouses, custodians, and banks all operate within that buffer. It is not inefficiency. It is a structural shock absorber built into how capital moves.

Atomic settlement removes that buffer entirely. When a trade settles instantaneously, every obligation - compliance verification, liquidity provision, counterparty confirmation, collateral posting - must be met at the moment of execution rather than distributed across a settlement cycle. The liquidity that the float window provided as a natural cushion must now be pre-positioned or instantly available. That is a fundamentally different risk architecture, and it hasn’t been stress-tested at an institutional scale under adverse conditions.

The 2023 USDC depeg illustrates one version of what adverse conditions look like for the cash leg. After Circle revealed it had nearly 8% of its $40 billion in reserves tied up at Silicon Valley Bank, USDC fell below 87 cents - a drop of more than 13 cents - over the weekend when primary market redemptions were constrained by the working hours of the US banking system.

The irony is precise: the banking infrastructure that atomic settlement is designed to move beyond was the only mechanism available to restore the peg. A regulated stablecoin with reserve requirements wouldn’t have prevented that event. It changes who bears the loss and under what framework.

The Fed is currently considering limited payment rail access for federally regulated stablecoin issuers - a “skinny” master account that would allow direct clearing and settlement in central bank money. That proposal is still under consideration. If on-chain settlement is atomic and the regulated stablecoin serving as the cash leg is simultaneously experiencing a redemption event, the settlement finality that the infrastructure promised and the liquidity the cash leg can deliver are no longer aligned. The float window that would have provided time to resolve that mismatch no longer exists. Has the legislation been written to govern this modeled scenario?

The Question That Stays Open

And then there is the question that survives even the best-case legislative scenario — the one worth sitting with regardless of where you sit in this market.

Consider what moved in the week this piece was written. The GENIUS Act rollout formally began on April 1st. The Federal Reserve, OCC, and FDIC issued their Basel III re-proposal on March 19th, retaining the 1,250% risk weight with a comment deadline of June 18th. The PARITY Act was updated and formally introduced on March 26. And today, April 3rd, the IMF published a comprehensive policy roadmap for integrating tokenized assets into the global financial architecture, with a core principle that “same activity, same risk, same regulation” must apply to tokenized versions of traditional securities. That is the right principle. It is also precisely what the current legislative stack - the CLARITY Act, PARITY Act, implementation of the GENIUS Act, and the two draft bills from March 25th, 2026 - cannot deliver, because the constraint stack spans tax law, prudential capital standards, and settlement infrastructure across jurisdictions that are not coordinating their responses.

Financial regulation has historically been built after the fact. Frameworks calibrated to the last crisis, applied to the next market, administered through oversight architectures designed for a world where innovation happened inside intermediaries that kept regular hours and filed regular reports. Tokenization is building infrastructure that is programmable, composable, and operates continuously across jurisdictions, without the natural pause points that traditional regulatory cycles depend on. The oversight framework being constructed around it is still episodic, jurisdiction-specific, and intermediary-dependent.

So the question that stays open after everything currently proposed passes is this: are we building a modern regulatory framework for tokenization, or are we building the most sophisticated version of a framework whose architecture was designed for a market that no longer exists? And if the answer is the latter, who bears the cost of that mismatch, and when does it become visible?

The answer to the last question is already known from the historical pattern. In every prior innovation cycle, the cost of framework mismatch concentrated farthest from the decision-making - in the clients who didn’t understand what they owned, the institutions that priced risk incorrectly because the framework didn’t require them to price it correctly, and the intermediaries who bore reputational costs for gaps in due diligence processes that nobody told them to build. The legislative activity of the past week confirms that Washington is engaged. It does not confirm that the architecture of oversight is being rebuilt for the market it is being asked to govern.

Those questions don’t have legislative answers yet. They may not have legislative answers at all in any timeframe the market currently operates on. What they have are the people building, allocating, and advising in this space right now, making architecture decisions that will determine whether their structures survive the moment those questions get answered the hard way.

The original observation holds: a signal for the market overall, and proof that legacy legislation has a long way to catch up. Both parts are correct. The signal is real. The distance is real. And the teams that are honest about how far the catch-up actually needs to go are the ones building on the right foundation for what comes after the bills that are currently moving eventually pass.

The RWA Ledger covers tokenization and the evolution of financial infrastructure toward more verifiable, on-chain systems. This analysis reflects publicly available legislative materials, testimony, market data, and primary sources as of March 31, 2026.